3 days ago

2

3 days ago

2

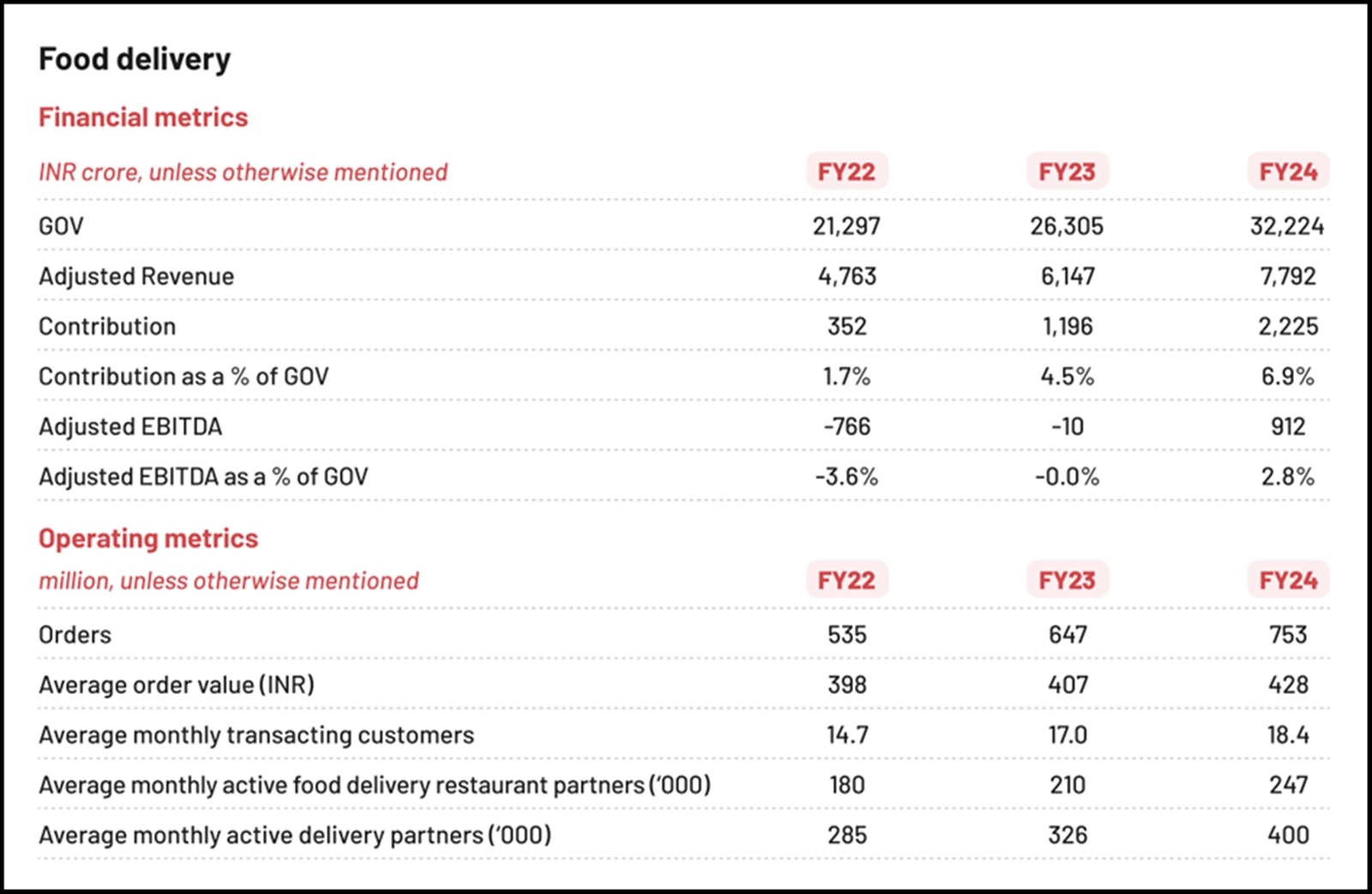

Zomato’s Food Delivery Business. (Source: Zomato’s Annual Report FY24)

Zomato’s Food Delivery Business. (Source: Zomato’s Annual Report FY24)

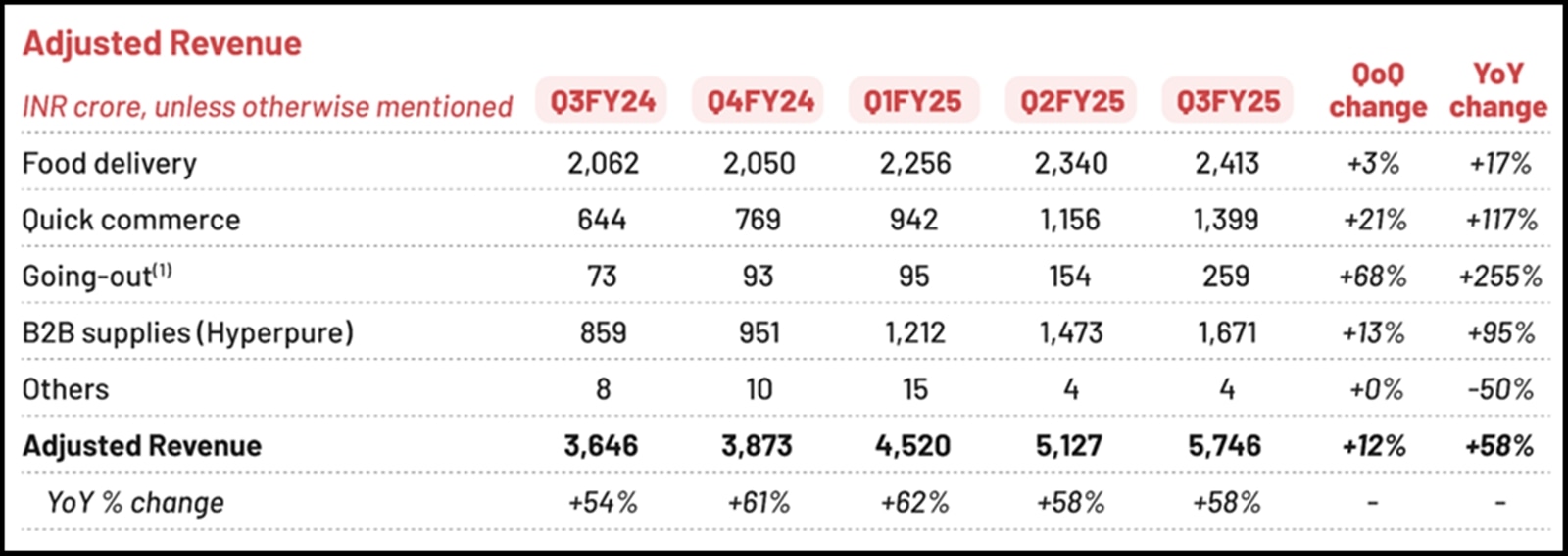

Zomato’s Revenue. (Source: Source: Zomato’s Q3FY25 Report)

Zomato’s Revenue. (Source: Source: Zomato’s Q3FY25 Report)

Zomato’s nutrient transportation concern has transitioned from accelerated enlargement to profitability. In Q3FY25, consolidated adjusted EBITDA grew a singular 128% YoY to ₹285 crore. The adjusted EBITDA margin, measured arsenic a percent of GOV, roseate to 4.3% successful Q3FY25 from 3.0% successful the aforesaid 4th a twelvemonth ago.

Platform Fee Optimisation: A humble summation successful lawsuit level fees contributed to improved margins.

Cost Efficiencies: Better logistics, little transportation costs, and reduced operational overheads added to profitability.

The institution has projected that adjusted EBITDA margins could stabilise astatine astir 5% successful the adjacent fewer quarters, signaling continued absorption connected efficiency.

Zomato is not contented with its existing playbook. It precocious launched 2 caller services:

Quick edifice delivery: Restaurants listed connected Zomato are present being enabled to present prime paper items successful nether 15 minutes, leveraging curated menus and dedicated fleets. This work is presently unrecorded successful prime cities, with plans for gradual scaling.

Bistro by Blinkit: Targeting firm offices, Bistro aims to code the untapped marketplace for speedy snacks, beverages, and meals. This inaugural is simply a strategical measurement into a marketplace traditionally served by vending machines and onsite vendors.

These innovations item Zomato’s absorption connected addressing niche markets portion enhancing lawsuit convenience.

The abbreviated answer: highly unlikely. Here’s why:

Steep superior barriers: The nutrient transportation marketplace has already seen implicit ₹56,000 crore ($7 billion) successful investments, chiefly betwixt Zomato and Swiggy. Matching this standard requires a hazard appetite that fewer caller entrants possess.

Network effects: Zomato’s relationships with 300,000+ restaurants and 200,000+ transportation partners make a competitory moat that would instrumentality years to replicate.

Customer loyalty: Zomato’s wide adoption, driven by loyalty programmes similar Zomato Gold, makes it hard for caller players to lure customers away.

For now, Zomato and Swiggy’s dominance seems unassailable, solidifying their positions arsenic the lone large players successful India’s nutrient transportation ecosystem.

The Indian nutrient transportation market, valued astatine ₹60,000 crore successful FY24, is projected to turn to ₹2 lakh crore by 2030, representing a compound yearly maturation complaint (CAGR) of 20%. If Zomato maintains its existent marketplace share, it could make revenues of ₹27,000 crore by 2030, assuming the instrumentality complaint holds dependable astatine 24%.

More importantly, EBITDA could standard 10x from existent levels to ₹5,500 crore, driven by operational efficiencies, higher AOVs, and optimised transportation costs.

While the nutrient transportation marketplace successful metros is maturing, Tier-2 and Tier-3 cities correspond the adjacent frontier for growth. Although these markets travel with challenges — little AOVs and higher transportation costs — they clasp immense imaginable arsenic integer adoption deepens crossed India.

Zomato’s foray into speedy commerce (Q-commerce) done Blinkit is 1 of the boldest bets successful India’s fast-evolving depletion landscape. Q-commerce emerged arsenic a solution to the inefficiencies of accepted market delivery, wherever delayed timelines and fragmented proviso chains near overmuch to beryllium desired.

Blinkit has taken the marketplace by storm, delivering bonzer growth, but profitability remains the elephant successful the room. The existent question is: Can Blinkit alteration into a habit-forming, profitable concern model?

‘Blink and You’ll Miss It’

The maturation successful Blinkit’s numbers is undeniable.

GOV leaped from ₹12,469 crore successful FY24 to ₹18,853 crore successful conscionable the archetypal 9 months of FY25.

By the extremity of FY25, Blinkit is projected to adjacent the twelvemonth astatine astir ₹26,000 crore successful GOV — a singular 124% yearly maturation rate. This trajectory has been powered by an assertive enlargement of acheronian stores, which service arsenic the backbone of its operations.

As of Q3FY25, Blinkit had 1,007 acheronian stores, and the institution has already revised its people of reaching 2,000 stores by December 2025 — a afloat twelvemonth up of earlier guidance.

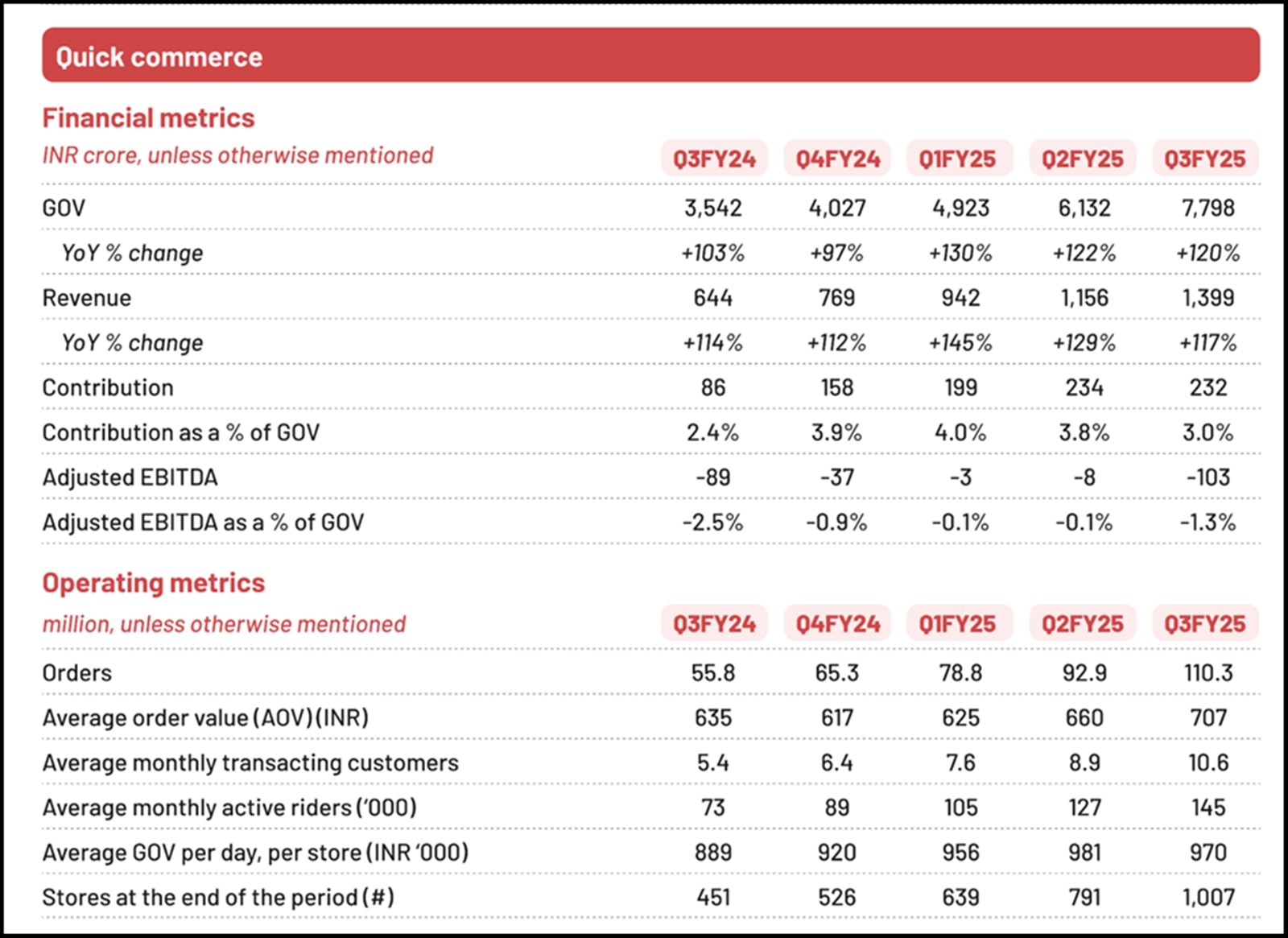

Source: Zomato’s Q3FY25 Report

Source: Zomato’s Q3FY25 Report

Profit oregon Loss?

What makes Q-commerce truthful compelling is its quality to code symptom points that accepted market transportation could not.

Blinkit has leveraged centralised acheronian stores, streamlining sourcing and reducing transportation times. This strategy, combined with India’s cost-effective labour market, has enabled it to execute transportation speeds that were antecedently unheard of.

Customers not lone worth velocity but are besides starting to presumption Blinkit arsenic a reliable level for mundane essentials, reinforcing a wont that could thrust aboriginal growth.

However, it’s not each creaseless sailing.

While Blinkit is increasing exponentially, profitability remains elusive. Contribution margins person turned positive, meaning the concern is covering its adaptable costs, but adjusted EBITDA remains successful the red.

In Q3FY25, the adjusted EBITDA borderline stood astatine -1.3% of GOV, a autumn from earlier quarters owed to the summation of caller stores. While 30% of Blinkit’s stores are already contribution-margin affirmative and lend implicit 50% of GOV, the newer stores are dragging down wide profitability.

Source: Source: Zomato’s Q3FY25 Report

Source: Source: Zomato’s Q3FY25 Report

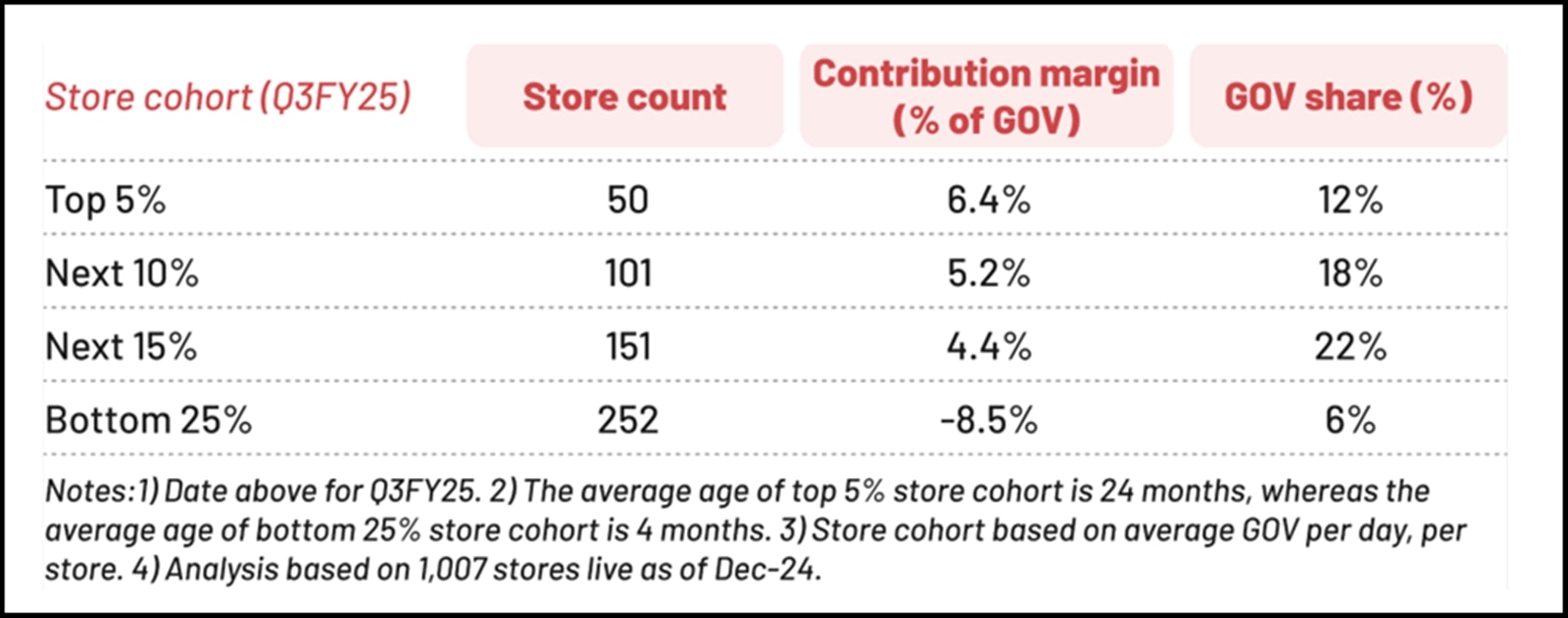

The nuances of Blinkit’s store cohort investigation uncover an absorbing pattern.

Older stores are highly profitable, with the apical 30% generating 52% of GOV and publication margins ranging from 4.4% to 6.4%.

These stores person had clip to mature, optimise operations, and physique a loyal lawsuit base. In contrast, the bottommost 25% of stores, which are newer and little established, run astatine antagonistic margins of -8.5%. This disparity underscores the situation of scaling Q-commerce portion maintaining fiscal discipline.

Yet, it besides hints astatine the imaginable for profitability if newer stores tin replicate the show of older cohorts.

Retention, attention, and store wars

The business’s idiosyncratic metrics further item its promise.

Blinkit’s GOV retention complaint is an astonishing 144%, meaning that the aforesaid users are spending much implicit time. AOV has risen from ₹625 successful Q1FY25 to ₹707 successful Q3FY25, signaling that customers are not lone ordering often but are besides placing higher-value orders.

This behavioural displacement suggests that Q-commerce is transitioning from a convenience-driven novelty to a profoundly ingrained habit.

The competitory landscape, however, is heating up.

While Blinkit and Swiggy Instamart person dominated the market, players similar Zepto, Flipkart, Amazon, and Reliance Retail are aggressively entering the fray.

Despite this, Blinkit has managed to outpace its competitors successful presumption of gross growth. Its revenues are 2.5x those of Instamart, owing to faster acheronian store enlargement and a much assertive concern strategy.

But the marketplace is not without limits. HDFC Securities estimates that India tin accommodate 7,500 acheronian stores, and with the apical players already operating adjacent to 6,000, the model for caller entrants is rapidly closing.

Blinking towards the decorativeness line

While challenges remain, the roadworthy to profitability is not wholly retired of reach.

If Blinkit’s existing trends clasp — particularly its precocious idiosyncratic retention, rising AOV, and the maturation of newer store cohorts — the concern could execute EBITDA profitability wrong six to 8 quarters. This is simply a important milestone that would solidify Blinkit’s spot arsenic a cardinal pillar of Zomato’s ecosystem.

What stands retired astir is however Blinkit has managed to foster wont enactment among its users. With customers returning often and spending more, Q-commerce is nary longer conscionable a solution to a problem; it is becoming a mode of life.

Building the adjacent pillars of growth

Zomato’s ongoing diversification has extended its scope into 2 promising verticals — its Going-Out Business and B2B Supplies. While inactive successful their aboriginal days, these segments clasp unsocial imaginable to make complementary ecosystems astir Zomato’s halfway nutrient transportation platform.

A nighttime out, reimagined: The going-out business

Launched successful November 2024, the District app is Zomato’s bold effort to consolidate India’s fragmented going-out market.

By integrating services similar dining-out, lawsuit ticketing, and amusement find nether a azygous platform, Zomato hopes to redefine however Indians prosecute with nightlife and taste events. Early signs are promising, with implicit 6.5 cardinal downloads wrong weeks of launch.

This initiative, however, comes with important challenges.

As Zomato transitions its going-out customers from platforms similar Paytm, Insider, and TicketNew to District, the absorption remains connected seamless idiosyncratic migration and improved engagement.

The institution aims to grow the platform’s selection, bringing world-class experiences to Indian audiences portion ensuring creaseless find done intuitive tech.

The financials archer a communicative of accelerated maturation paired with dense investment.

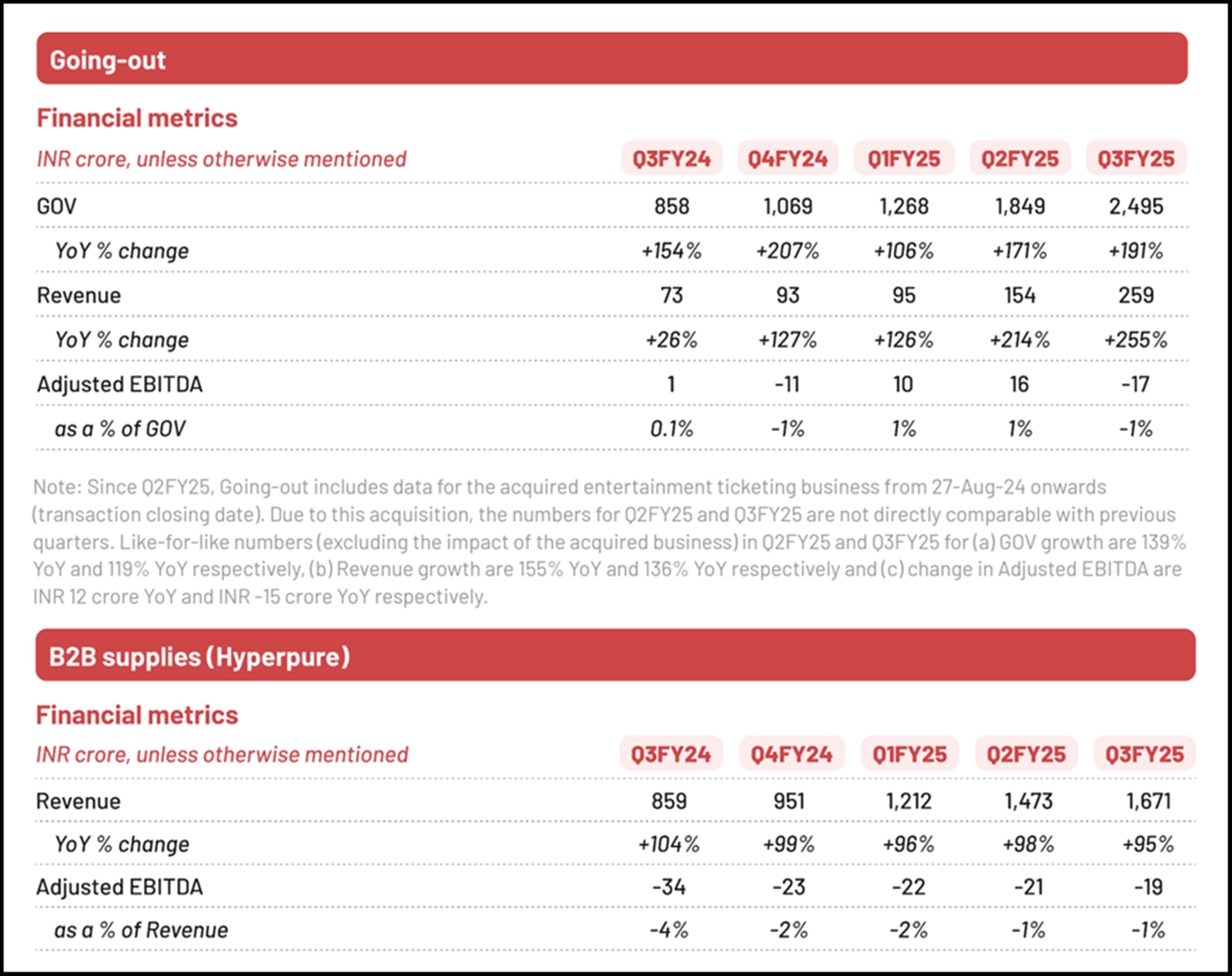

In Q3FY25, the going-out vertical generated a GOV of ₹2,495 crore, marking a 191% YoY increase. Revenue for the conception jumped 255% YoY to ₹259 crore. However, adjusted EBITDA fell to ₹-17 crore for the quarter, driven by expenses related to District’s development, marketing, and squad expansion.

While profitability is not expected successful the adjacent term, the halfway going-out concern remains profitable extracurricular of these investments. Zomato is betting that the enhanced lawsuit acquisition connected District volition wage dividends implicit time, establishing it arsenic a one-stop destination for each going-out activities successful India.

Zomato’s Going-out, Hyperpure Business. (Source: Zomato’s Q3FY25 Report)

Zomato’s Going-out, Hyperpure Business. (Source: Zomato’s Q3FY25 Report)

B2B Supplies: A quiescent but dependable maturation engine

Zomato’s B2B Supplies concern has a simpler narrative: it exists to enactment restaurants, chiefly by providing indispensable goods and services.

As India’s edifice scenery grows, this vertical people benefits from accrued request for room supplies, earthy materials, and operational tools.

Although it is improbable to rival the standard of Zomato’s different businesses, B2B supplies play a captious relation successful strengthening the company’s narration with restaurants. By streamlining procurement, Zomato helps its partners trim costs, amended efficiency, and absorption connected delivering prime eating experiences.

This symbiotic narration not lone bolsters the edifice ecosystem but besides reinforces Zomato’s presumption arsenic a cardinal enabler successful the nutrient industry.

For now, the conception is expected to stay tiny but resilient. Its maturation volition reflector the emergence of caller restaurants, making it a complementary, if understated, portion of Zomato’s wide strategy.

Should 1 put successful Zomato?

Zomato’s existent marketplace capitalization hovers astir ₹2 lakh crore aft a caller rerating implicit the past 2 weeks.

With a Price-to-Sales (P/S) ratio of astir 9x based connected trailing 12-month revenue, the banal is trading astatine a premium compared to planetary peers successful the nutrient and transportation space. This premium is mostly driven by Zomato’s beardown marketplace stock successful nutrient transportation (55%), its enactment successful speedy commerce done Blinkit, and its quality to prolong gross maturation adjacent arsenic contention intensifies.

For FY24, Zomato reported full gross of ₹13,545 crore, representing a 56% YoY growth. Analysts task revenues to surpass ₹25,000 crore by FY26, driven by continued enlargement successful nutrient transportation and speedy commerce.

Assuming Zomato maintains its existent valuation multiple, the marketplace capitalization could spot a imaginable upside of 50% from existent levels, driven by its beardown maturation trajectory and expanding verticals.

However, profitability remains the cardinal concern.

While the company’s adjusted EBITDA turned affirmative for its halfway nutrient transportation business, the dense investments successful Blinkit and the District app person weighed connected consolidated profitability.

Blinkit, for instance, is projected to execute EBITDA profitability wrong the adjacent six to 8 quarters, with an expected gross publication of implicit ₹20,000 crore by FY30. Similarly, the going-out concern is poised to turn astatine a 40%+ CAGR implicit the adjacent fewer years, albeit with near-term losses arsenic District scales.

With a beardown equilibrium expanse and nary contiguous request for further capital, Zomato is well-positioned to money these expansions. However, the modulation from maturation to profitability volition necessitate disciplined execution. Any misstep — whether successful scaling caller verticals oregon maintaining lawsuit loyalty successful nutrient transportation — could measurement heavy connected the stock’s valuation.

The last word

Zomato’s communicative is 1 of translation and ambition.

It has successfully diversified its concern portion maintaining enactment successful its halfway operations. The company’s absorption connected creating an integrated ecosystem, combined with its beardown execution way record, makes it an breathtaking imaginable for growth-oriented investors.

However, the stock’s premium valuation leaves small country for error.

While the semipermanent maturation imaginable is evident, the travel to sustainable profitability and the quality to fend disconnected intensifying contention volition find its eventual success. Investors should measurement the maturation opportunities against the execution risks and see their ain hazard tolerance earlier making immoderate decisions.

As Zomato navigates its adjacent signifier of growth, it remains a institution to ticker — some for its strategical moves and its quality to redefine India’s integer depletion landscape.

Note: We person relied connected information from the yearly reports passim this article. For forecasting, we person utilized our assumptions.

Parth Parikh has implicit a decennary of acquisition successful concern and research, and helium presently heads the maturation and contented vertical astatine Finsire. He has a keen involvement successful Indian and planetary stocks and holds an FRM Charter on with an MBA successful Finance from Narsee Monjee Institute of Management Studies. Previously, helium has held probe positions astatine assorted companies.

Disclosure: The writer and his dependents bash not clasp the stocks discussed successful this article.

The website managers, its employee(s), and contributors/writers/authors of articles person oregon whitethorn person an outstanding bargain oregon merchantability presumption oregon holding successful the securities, options connected securities oregon different related investments of issuers and/or companies discussed therein. The contented of the articles and the mentation of information are solely the idiosyncratic views of the contributors/ writers/authors. Investors indispensable marque their ain concern decisions based connected their circumstantial objectives, resources and lone aft consulting specified autarkic advisors arsenic whitethorn beryllium necessary

.png "indianexpress.")

.png "khaleejtimes")

.png "arabnews")

English (US) ·

English (US) ·  Hindi (IN) ·

Hindi (IN) ·