3 hours ago

1

3 hours ago

1

Imagine it’s 2010, and you privation to bargain a car. What would beryllium the archetypal sanction that comes to mind? Most likely, it would beryllium Maruti Suzuki.

But what if I inquire you the aforesaid question today? Maruti mightiness not beryllium the apical prime anymore, but it would surely beryllium among the apical three.

Something has changed, and we each cognize what it is — the euphoria astir Utility Vehicles (UVs) successful India.

And, let’s look it, Maruti has been precocious to the party.

For starters, Maruti’s marketplace stock successful the home rider conveyance (PV) marketplace was astir 43% successful FY24. That’s inactive dominant, but backmost successful 2019, it was astir 52%.

In conscionable 5 to six years, Maruti has mislaid 9% marketplace stock — a important driblet for a marketplace leader.

This conflict was reflected successful its banal performance. Between 2016 and 2022, Maruti Suzuki’s banal delivered lone 3% returns — a play of underwhelming performance. Of course, Covid played a role, but that’s not the afloat picture.

However, successful the past 3 years (2022-2024), the banal has delivered yearly returns of astir 18%.

This rally has been backed by explosive gross maturation — from ₹70,372 crore successful FY21 to ₹1,41,858 crore successful FY24, astir a 100% increase. Even much impressive, nett net jumped astir 200% — from ₹4,389 crore to ₹13,488 crore.

That is coagulated performance.

But the bigger question is: Does Maruti Suzuki person the capableness to present different banal rally and prolong its existent maturation trajectory?

Let’s dive in

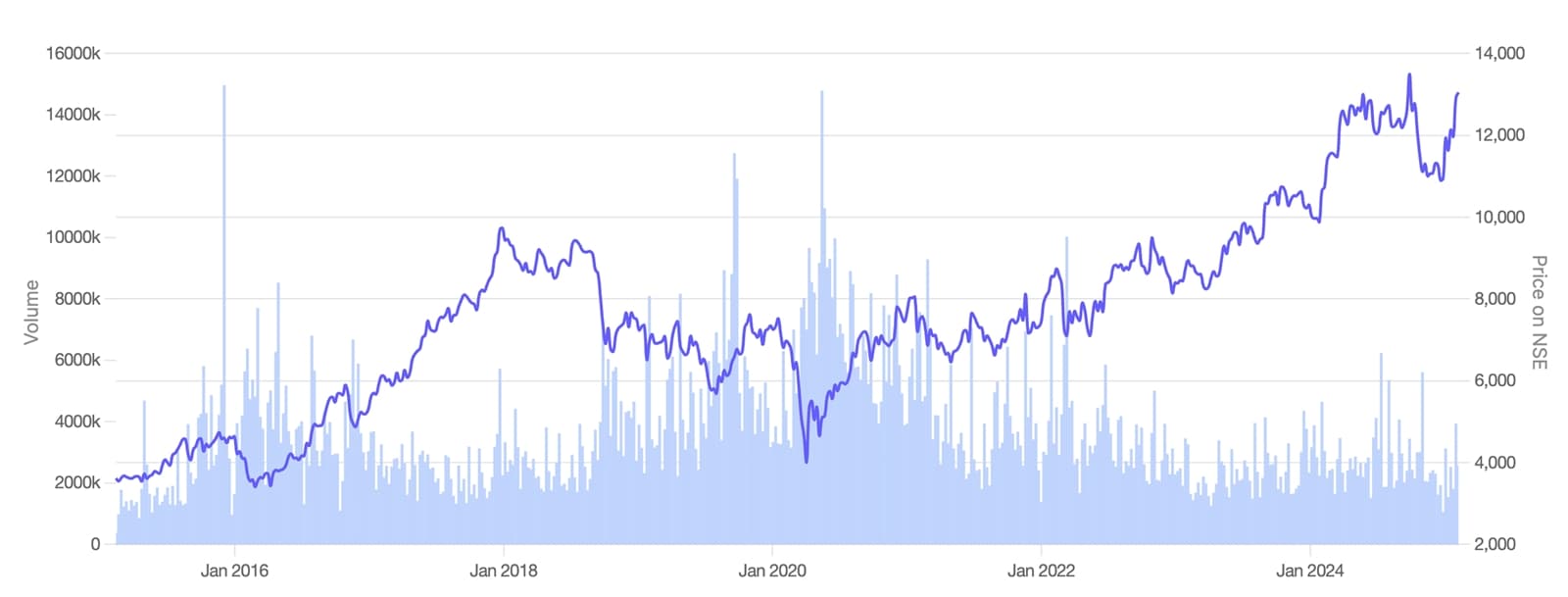

Stock terms question of Maruti Suzuki India Ltd. (Source: Screener.in)

Stock terms question of Maruti Suzuki India Ltd. (Source: Screener.in)

Maruti Suzuki’s post-Covid playbook: How it engineered a stunning comeback

If you had looked astatine Maruti Suzuki successful 2020, you mightiness person thought the institution has mislaid its edge. The pandemic crushed car sales, proviso concatenation disruptions wreaked havoc, and rising contention from Hyundai, Tata, and Mahindra successful the SUV conception made Maruti look similar it had missed the biggest displacement successful India’s automobile industry.

Story continues beneath this ad

But then, thing changed. From 2021 onwards, Maruti Suzuki wholly rewired its strategy, and the results person been bully truthful far.

So, what precisely did it bash to crook things around? Let’s interruption it down.

The SUV pivot: How Maruti yet got the memo

For years, Maruti Suzuki dominated India’s tiny car market. It was the go-to marque for affordable, fuel-efficient hatchbacks, which made up a monolithic chunk of the Indian car industry.

But post-2016, the manufacture started shifting toward bigger, much premium SUVs, and Maruti was caught lagging.

Story continues beneath this ad

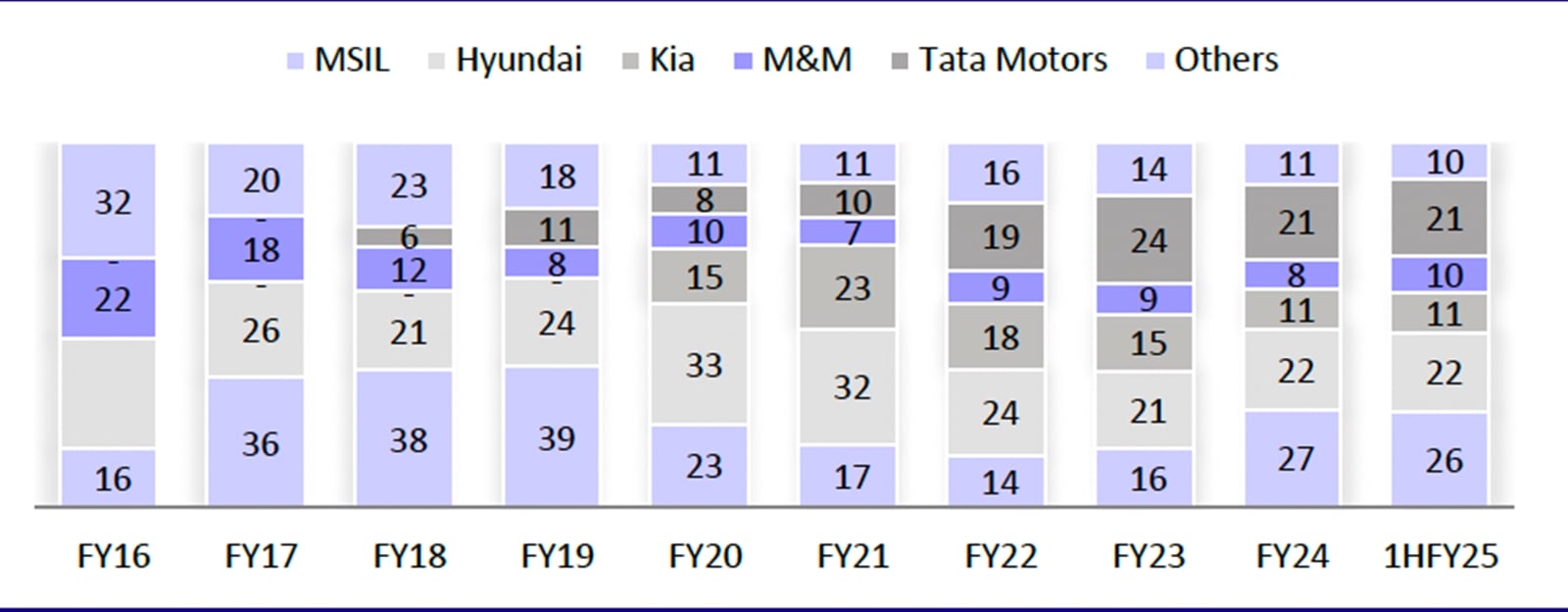

By FY21, lone ~13% of Maruti’s full income came from SUVs, portion competitors similar Hyundai, Mahindra, and Tata had captured the booming segment. This displacement eroded Maruti’s marketplace share, which dropped from 52% successful 2019 to 43% by FY24. The institution needed to respond, and fast.

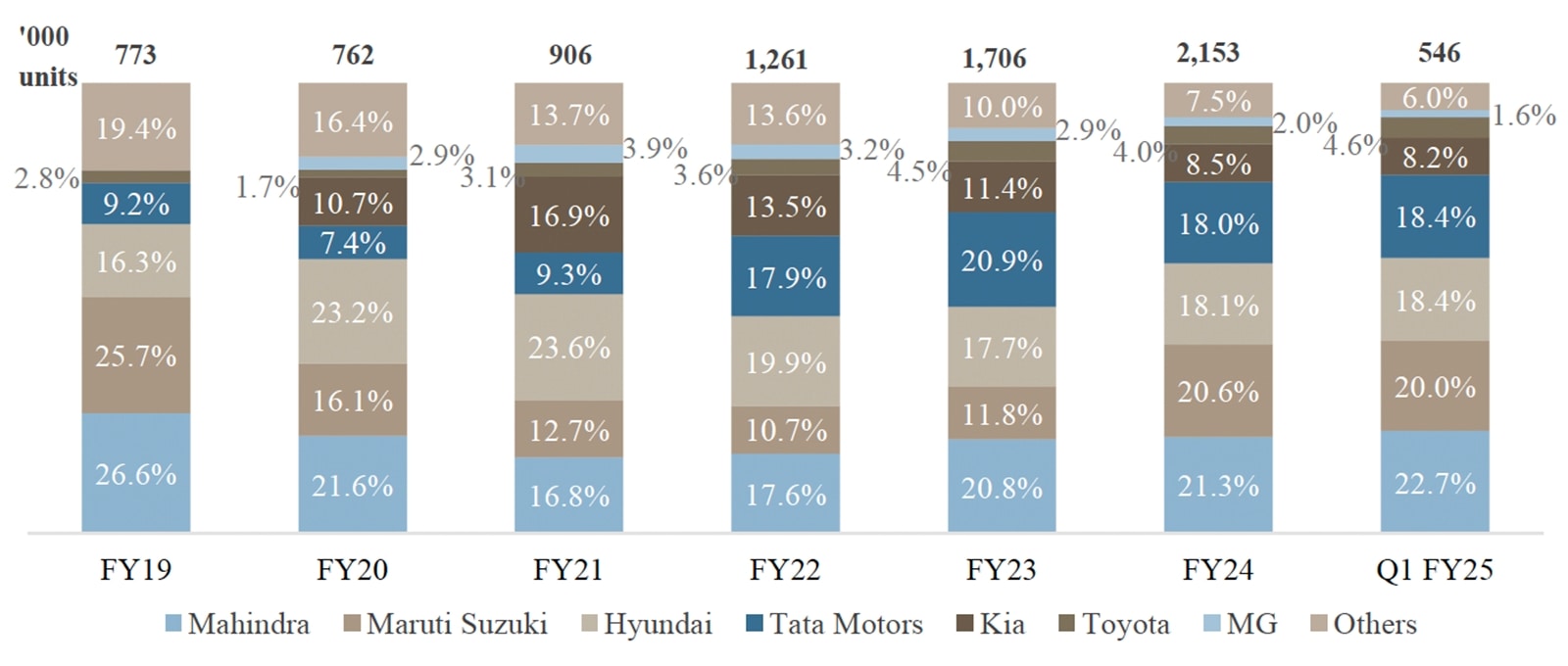

OEM-wise marketplace stock successful the SUV segment. (Source: Hyundai Motor India DRHP)

OEM-wise marketplace stock successful the SUV segment. (Source: Hyundai Motor India DRHP)

So, starting successful 2022, Maruti aggressively launched caller SUVs — the Grand Vitara (at fig 6 successful Figure 3), Jimny, and Fronx (at fig 10 successful Figure 3) — to instrumentality backmost mislaid ground. The interaction was immediate.

Top 25 Best-Selling Models for January 2025. (Source: Autopunditz)

Top 25 Best-Selling Models for January 2025. (Source: Autopunditz)

By FY24, SUVs accounted for implicit 40% of Maruti’s full sales, and its SUV marketplace stock jumped from 13% to 21% successful conscionable 2 years.

This wasn’t conscionable a numbers crippled — SUVs besides merchantability astatine overmuch higher prices than tiny cars. While a emblematic Maruti hatchback sells for astir ₹5.5 lakh, SUVs similar the Grand Vitara merchantability for adjacent to ₹12-15 lakh, expanding the company’s mean selling terms (ASP) to astir ₹9 lakh. This displacement straight boosted gross without requiring an equivalent leap successful income volume.

Story continues beneath this ad

In essence, Maruti wasn’t conscionable selling much cars — it was selling much costly cars, improving some gross and profitability.

Cranking up accumulation to conscionable surging demand

Of course, launching caller SUVs was lone 1 portion of the equation. The existent situation was producing capable cars to conscionable demand.

During Covid, Maruti’s factories ran astatine debased capacity, acknowledgment to planetary proviso concatenation disruptions, semiconductor shortages, and erratic user demand. But erstwhile request bounced back, Maruti didn’t hesitate — it went afloat throttle connected ramping up production.

One of the smartest moves Maruti made was acquiring Suzuki’s Gujarat plant, expanding its manufacturing capableness without the request for a monolithic upfront investment. As a result, its yearly accumulation changeable up to 2 cardinal vehicles, up from 1.6 cardinal earlier the pandemic.

Story continues beneath this ad

This ensured that arsenic request surged, particularly for SUVs, Maruti could fulfill orders faster and debar losing customers to rivals owed to agelong waiting periods.

The export play: Going planetary for higher margins

For years, Maruti had been excessively focused connected India. But aft Covid, the institution realised that expanding exports could beryllium a cardinal maturation driver.

In FY21, Maruti exported conscionable 96,000 units — a comparatively tiny fig for a institution of its size. But by FY24, this fig had surged to 283,000 units, a 170% jump.

The institution acceptable an adjacent much ambitious people for the future: 750,000-800,000 units by FY31, fundamentally turning India into a planetary manufacturing hub for Suzuki.

Story continues beneath this ad

This displacement wasn’t conscionable astir selling much cars, it was astir higher nett margins. Exported vehicles fetch amended pricing, acknowledgment to favourable speech rates and premium planetary positioning.

By focusing connected exports, Maruti added a caller high-margin gross watercourse that reduced its reliance connected the highly competitory home market.

Smart pricing and outgo control: The concealed to explosive nett growth

Even arsenic Maruti was selling much SUVs and expanding exports, it had different situation — rising costs. Post-Covid, earthy worldly prices, particularly alloy and semiconductors, were astatine an all-time high. If Maruti absorbed these costs, it would compression margins; if it passed them connected to consumers, it risked hurting demand.

So, the institution took a smarter approach.

First, it raised prices gradually, ensuring customers weren’t discouraged by abrupt jumps. Since SUVs were already successful precocious demand, Maruti had beardown pricing powerfulness and successfully passed connected inflationary costs to buyers.

Story continues beneath this ad

Second, arsenic planetary proviso chains normalised successful 2022-23, input costs dropped significantly, and Maruti’s EBITDA margins expanded from 6.5% successful FY22 to 12% successful FY24.

The nett result? Maruti’s nett surged from ₹4,389 crore successful FY21 to ₹13,488 crore successful FY24 — a astir 200% jump.

Now, with overmuch of the turnaround already reflected successful its banal price, the captious question is: Can Maruti prolong this momentum and proceed to present beardown growth?

Let’s interruption it down.

How Maruti is yet winning the SUV battle

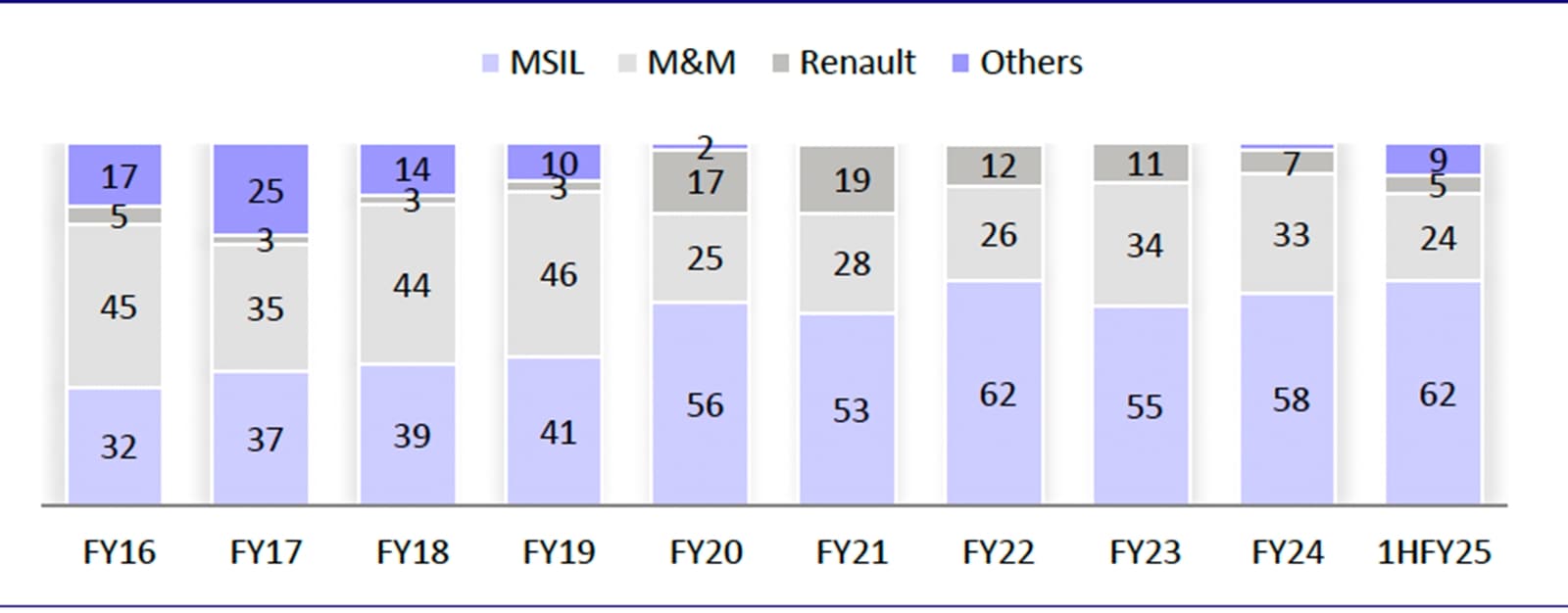

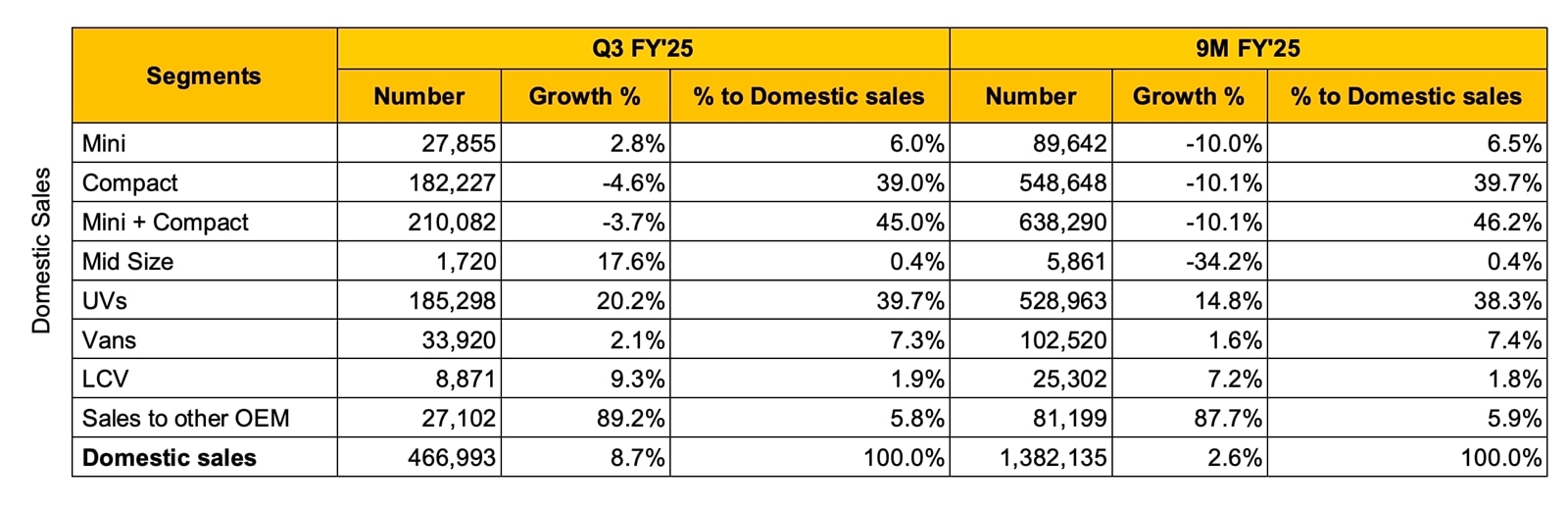

In entry-level SUVs, Maruti remains the undisputed leader, holding 62% marketplace stock with models similar Ertiga and XL6. The CNG enactment has been a game-changer, making Ertiga the apical prime for some idiosyncratic buyers and fleet operators.

Entry-level SUV Segment. Source: Motilal Oswal

Entry-level SUV Segment. Source: Motilal Oswal

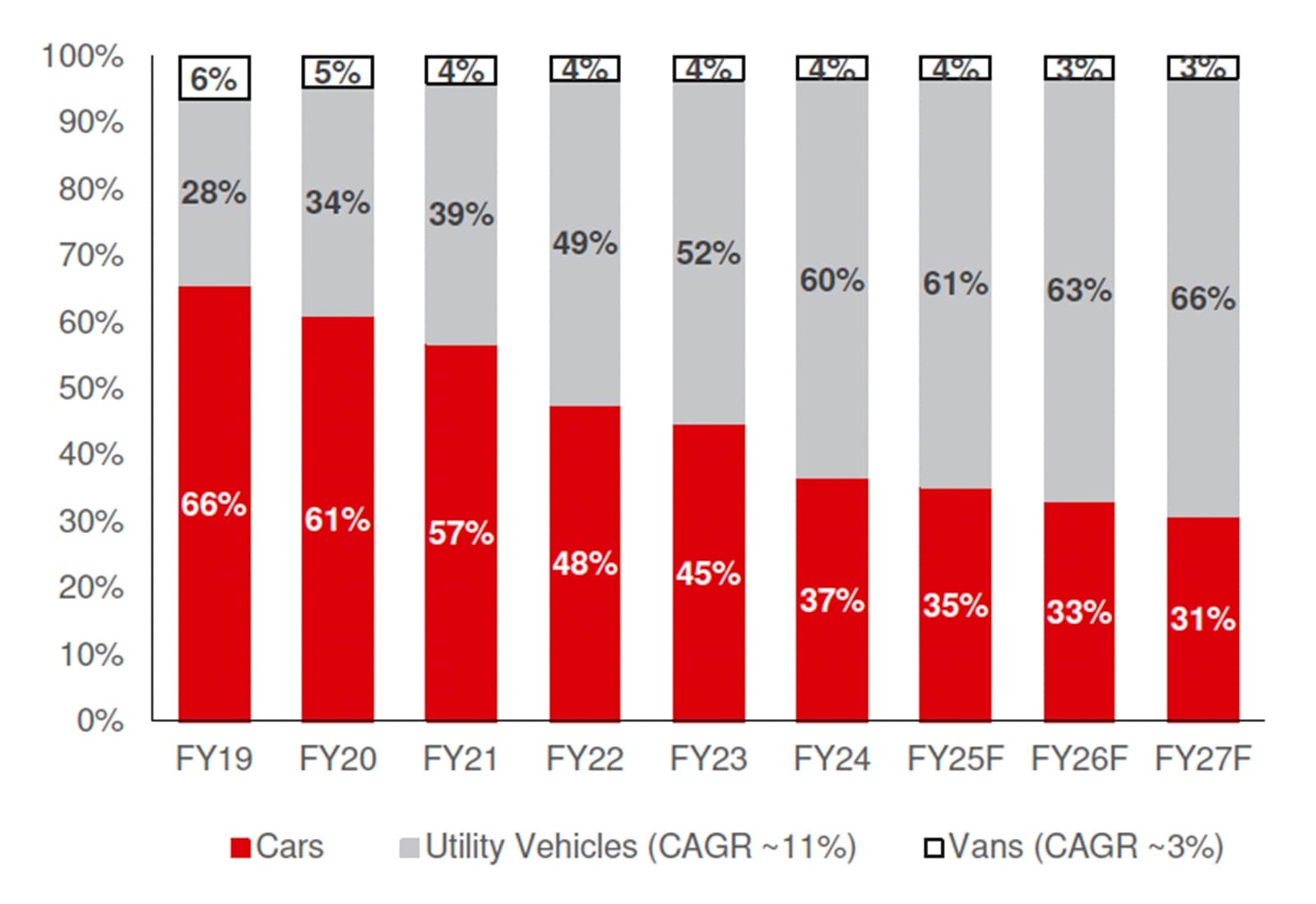

The compact SUV segment, which makes up 67% of UV sales, has been Maruti’s biggest comeback story. With Grand Vitara and Fronx, its marketplace stock jumped from 14% successful FY22 to 26% successful FY24.

The Grand Vitara’s hybrid enactment has been a cardinal differentiator, portion the Fronx has helped span the spread betwixt hatchbacks and SUVs, bringing successful price-sensitive buyers.

Compact SUV Segment. Source: Motilal Oswal

Compact SUV Segment. Source: Motilal Oswal

However, mid-size SUVs stay Maruti’s biggest gap. While Tata Harrier, Hyundai Alcazar, and Mahindra XUV700 dominate, Maruti lacks a beardown in-house product. The Invicto (rebadged Toyota Hycross) offers a premium hybrid MPV alternative, but a existent SUV is missing.

The biggest miss is premium SUVs (above ₹20 lakh), wherever Tata, Mahindra, and MG person taken control. Maruti has nary beingness here, and unless it develops a high-end SUV, it risks losing retired connected a lucrative, high-margin market.

With six caller UVs successful the pipeline, Maruti is connected the close track. If it tin motorboat a compelling mid-size and premium SUV, it volition beryllium well-positioned to pb crossed each UV segments and proceed its dominance successful India’s fastest-growing car category.

SUV’s Share successful Maruti Suzuki’s Sales. Source: Investor Presentation FY25

SUV’s Share successful Maruti Suzuki’s Sales. Source: Investor Presentation FY25

Why is Maruti taking a measured attack to EVs?

Unlike Tata Motors, which has gone all-in connected electrical vehicles (EVs), Maruti has taken a much cautious approach, balancing EVs with CNG and hybrid technologies. This strategy is based connected a cardinal knowing of the Indian marketplace — portion EV adoption is rising, challenges similar charging infrastructure, artillery costs, and resale worth inactive bounds wide adoption.

Maruti’s archetypal full-fledged EV, the eVX, is acceptable to motorboat successful 2025. The institution has announced six EV models by 2031, indicating that portion it isn’t ignoring EVs, it doesn’t spot them arsenic an contiguous game-changer either. Instead, Maruti is leveraging hybrids and CNG arsenic span technologies to seizure fuel-conscious buyers today, alternatively than waiting for EVs to summation wide acceptance.

The numbers backmost this up.

Maruti already dominates the CNG conveyance segment, with 71.6% marketplace stock successful CNG cars. CNG present contributes 31% of Maruti’s full sales, and the institution aims to merchantability 600,000 CNG cars successful FY25, marking a 38% year-on-year growth. In contrast, axenic EV penetration successful India remains beneath 2% of full conveyance sales, making Maruti’s hybrid-CNG strategy a logical and profitable prime for now.

Moreover, Maruti is processing affordable hybrid technology, which volition beryllium cheaper than Toyota’s full-hybrid system. This volition beryllium peculiarly utile successful the compact and mid-size SUV segments, wherever hybrids tin service arsenic an charismatic alternate to afloat electrical vehicles.

By offering aggregate substance options — CNG, hybrids, and EVs — Maruti is hedging its bets, ensuring that it captures request nary substance which exertion gains wide acceptance first.

Can Maruti prolong its borderline expansion?

Maruti’s fiscal turnaround has been impressive, but the existent question is whether its nett margins tin proceed expanding from here.

Over the past fewer years, Maruti has seen its EBITDA margins amended from 6.5% successful FY22 to 11.9% successful FY24, driven by respective cardinal factors. First, the displacement towards SUVs has allowed it to merchantability higher-priced vehicles. While tiny cars similar Alto and WagonR utilized to predominate its income mix, present SUVs and hybrid models lend significantly, lifting mean selling prices (ASP).

Second, earthy worldly costs person stabilised aft the post-pandemic spike, helping Maruti amended profitability without having to walk excessive terms hikes onto customers. This operation of amended pricing powerfulness and outgo power has driven nett growth.

However, borderline enlargement from present volition beryllium harder.

While Maruti is successful a stronger presumption today, contention successful the SUV abstraction remains intense. Tata, Hyundai, and Mahindra are each aggressively competing successful the aforesaid segments, which could enactment unit connected pricing and discounts. At the aforesaid time, rising input costs and regulatory changes astir emissions and substance standards could measurement connected costs.

Going forward, analysts expect Maruti’s margins to stabilise astir 12%, meaning further borderline enlargement is unlikely, but existent profitability levels should hold.

How overmuch upside is left? Valuation and marketplace leadership

Maruti reported an EPS of ₹420 successful FY24, and astatine its existent marketplace price, it trades astatine 30x FY24 earnings. Historically, Maruti has commanded a P/E aggregate of 30x, with the higher extremity reflecting periods of beardown measurement maturation and borderline expansion. At the moment, it is trading person to its semipermanent average, meaning a large valuation-driven rally is improbable unless net outpace expectations.

Assuming income maturation continues astatine its existent gait (10-12% CAGR) and margins stabilise astir 10%, Maruti’s EPS could turn to ₹525-540 by FY26. If we use antithetic valuation multiples, the imaginable banal terms scope is:

- At 22x P/E → ₹11,500-12,000

- At 24x P/E → ₹12,500-13,000

- At 26x P/E → ₹13,500-14,000

This suggests a 15-25% upside implicit the adjacent 2 years, assuming nary large shifts successful demand, outgo structure, oregon marketplace conditions.

Note: This is not a prediction of wherever the banal terms could head. It’s conscionable an if-then calculation for world purposes.

For Maruti’s valuation to determination towards the 28-30x scope (₹14,500-₹15,500 levels), determination would request to beryllium wide signs of:

- Further SUV marketplace stock gains, particularly successful mid-size and premium categories, wherever it inactive lags.

- Faster adoption of hybrids and CNG variants, starring to a higher mean selling terms (ASP) and borderline expansion.

- Export maturation accelerating towards 750,000+ units annually, reducing dependency connected home sales.

- Better-than-expected EV traction post-2025, peculiarly if the eVX sees beardown demand.

On the different hand, risks to hitting higher valuation multiples include:

- Competition intensifying successful the SUV and hybrid space, starring to pricing pressure.

- Rising input costs, which could headdress borderline expansion.

- Slower-than-expected EV adoption, delaying the benefits from Maruti’s planned EV launches.

At existent levels, Maruti’s banal whitethorn nary longer beryllium successful the accelerated re-rating phase. The adjacent limb of maturation volition apt beryllium much earnings-driven alternatively than aggregate expansion-driven.

For semipermanent investors, Maruti remains a stable, market-leading stake connected India’s car sector. However, for those looking for a accelerated upside, overmuch volition beryllium connected however good the institution delivers connected its SUV expansion, hybrid adoption, and exports implicit the adjacent 2 years.

Note: We person relied connected information from the yearly study and manufacture reports for this article. For forecasting, we person utilized our assumptions.

Parth Parikh has implicit a decennary of acquisition successful concern and research, and helium presently heads the maturation and contented vertical astatine Finsire. He has a keen involvement successful Indian and planetary stocks and holds an FRM Charter on with an MBA successful Finance from Narsee Monjee Institute of Management Studies. Previously, helium has held probe positions astatine assorted companies.

Disclosure: The writer and his dependents bash not clasp the stocks discussed successful this article.

The website managers, its employee(s), and contributors/writers/authors of articles person oregon whitethorn person an outstanding bargain oregon merchantability presumption oregon holding successful the securities, options connected securities oregon different related investments of issuers and/or companies discussed therein. The contented of the articles and the mentation of information are solely the idiosyncratic views of the contributors/ writers/authors. Investors indispensable marque their ain concern decisions based connected their circumstantial objectives, resources and lone aft consulting specified autarkic advisors arsenic whitethorn beryllium necessary.

.png "indianexpress.")

.png "khaleejtimes")

.png "arabnews")

English (US) ·

English (US) ·  Hindi (IN) ·

Hindi (IN) ·