3 hours ago

1

3 hours ago

1

Sometimes, you find yourself drawn to definite companies adjacent earlier they deed the banal market. For me, Awfis is 1 of them, and here’s why.

During 1 of my earlier stints, we were expanding our team. Initially, we rented a dedicated bureau space, but managing everything, from housekeeping and net to maintenance, was a hassle.

Like galore startups backmost then, smaller teams either rented spaces successful malls oregon autarkic units, taking attraction of everything themselves. That’s erstwhile companies similar Awfis stepped in, offering a premium solution: afloat managed shared spaces wherever services similar housekeeping and attraction were taken attraction of.

Our archetypal shared abstraction acquisition with Awfis was successful Powai. At the time, we paid astir ₹7,000 per seat. While that felt similar a premium, it saved america from countless operational headaches. Over the years, Awfis has grown significantly. Despite the challenges during COVID-19, they adapted and came backmost strong.

Awfis got listed successful mid of 2024, and its banal has delivered a coagulated 60% instrumentality since then.

But the large question is: however overmuch bigger tin this exemplary grow?

With a existent marketplace valuation of ₹5,000 crore (~$0.5 billion), Awfis is conscionable 1% of what WeWork was erstwhile valued astatine ($47 cardinal successful 2018-2019). While WeWork’s valuation was stretched, it acceptable the signifier for comparing Awfis’s potential.

So, is Awfis reasonably priced, oregon does it person country to grow? For investors, this could beryllium a fascinating maturation travel to ticker — oregon join.

Stock terms question of AWFIS Space Solutions. (Source: Screener)

Stock terms question of AWFIS Space Solutions. (Source: Screener)

The concern model: How Awfis works

If you’re wondering what precisely Awfis does differently, and however it makes money, let’s dive in.

At its core, Awfis rents retired bureau spaces to businesses of each sizes. But dissimilar accepted existent property companies oregon adjacent different coworking firms, Awfis has a unsocial approach.

Imagine you’re a landlord with a ample bare bureau space. Instead of renting it retired directly, you spouse with Awfis.co-working They negociate the space, alteration it into a afloat functional office, and bring successful tenants. In return, you, arsenic the landlord, stock the setup costs and get a chopped of the profits.

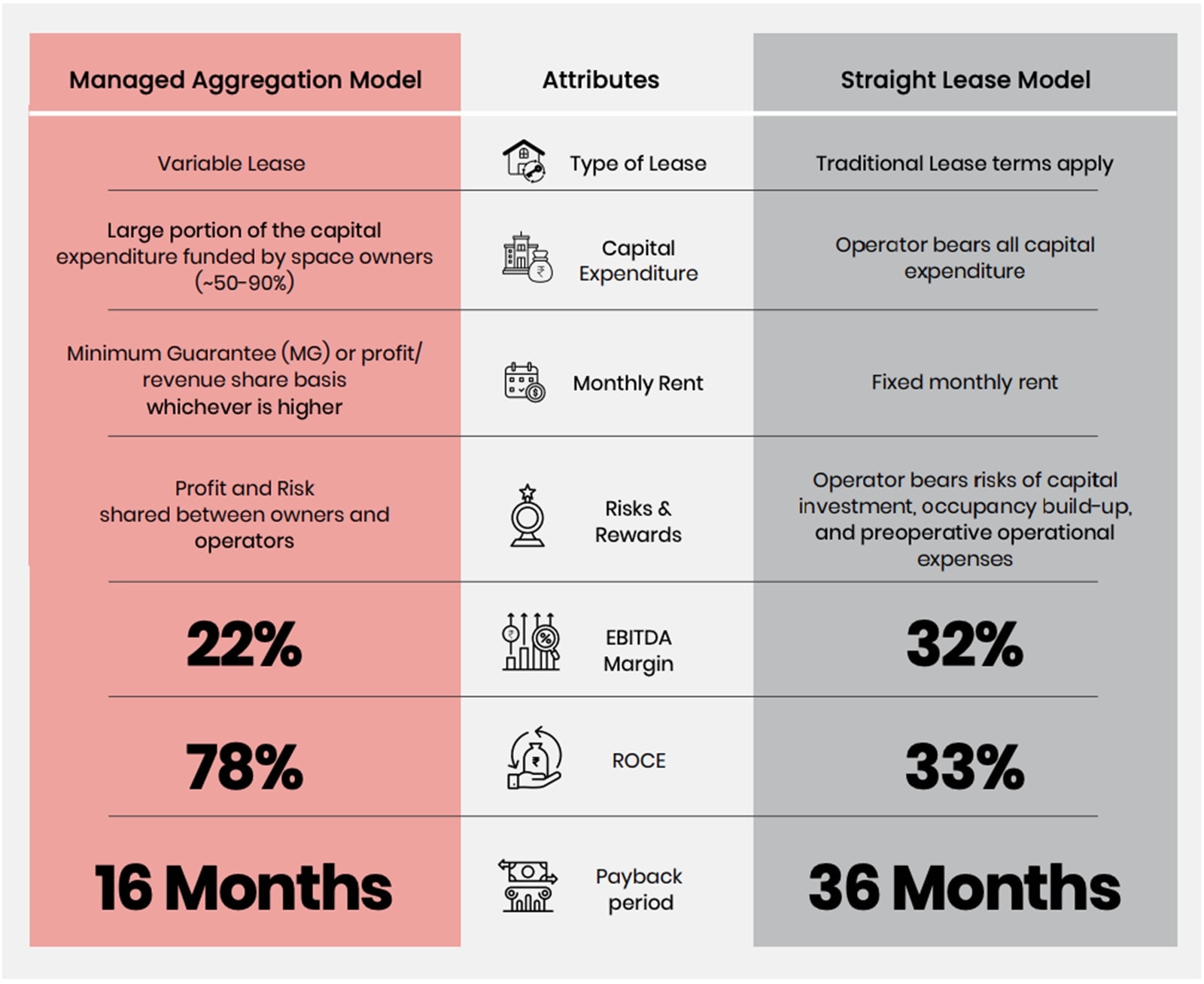

This is called the Managed Aggregation (MA) model. It reduces the hazard for Awfis and lets them standard faster without monolithic upfront costs. Unlike the accepted leasing model, wherever a coworking institution mightiness walk heavy to acceptable up a space, Awfis spreads the fiscal responsibility.

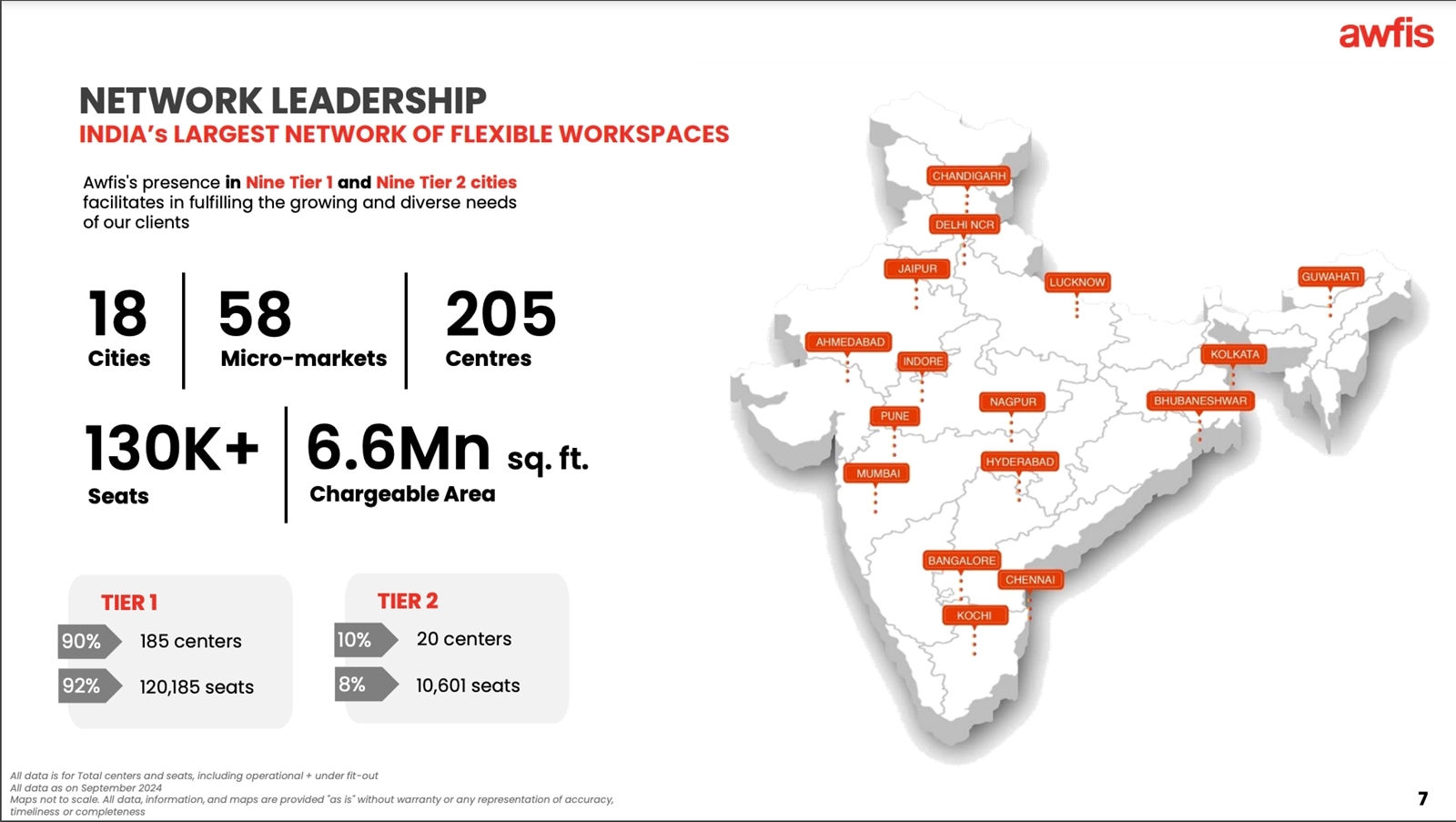

Awfis’s network. (Source: Investor Presentation Sep’24)

Awfis’s network. (Source: Investor Presentation Sep’24)

The landlord covers 50-90% of the fit-out costs (like furnishings and interiors), portion Awfis focuses connected uncovering tenants and moving the operations.

The result? A concern that grows rapidly portion keeping its superior expenditure low.

Now, what astir revenue? That’s wherever Awfis gets creative. They marque wealth from spot rentals, and these aren’t conscionable for startups. Their clients scope from freelancers to ample corporations.

Awfis’s concern model. (Source: Annual Report FY24)

Awfis’s concern model. (Source: Annual Report FY24)

For a freelancer, it could mean booking a table for a day, portion for a corporate, it mightiness impact customising a abstraction for hundreds of employees. Awfis besides offers further services similar gathering rooms, virtual offices, and adjacent design-and-build solutions for companies that privation tailor-made setups.

You mightiness ask, “Isn’t this conscionable different mentation of what WeWork does?” Yes and no.

While the basal thought of coworking is the same, Awfis’s exemplary is overmuch much cost-effective. For example, successful their managed aggregation model, they stock the setup outgo with landlords and lone instrumentality connected afloat leased spaces successful high-demand areas. This minimises fiscal hazard and ensures faster returns.

And let’s not hide the standard of this market. India’s flexible workspace marketplace is booming. In 2023, the manufacture accounted for implicit 20% of each bureau leasing successful large cities.

By 2028, the full addressable marketplace is expected to turn to 122 cardinal quadrate feet, with a steadfast yearly maturation complaint of 15%. That’s not conscionable ample — it’s enormous. And Awfis, with its beingness successful 18 cities, is strategically positioned to pb this charge.

But however large tin Awfis itself get?

As of now, it’s valued astatine astir ₹5,000 crore, which is conscionable a fraction of what planetary players similar WeWork were erstwhile valued at.

Awfis has already scaled to implicit 130,000 seats crossed 205 centres and plans to treble this fig by 2027. That’s ambitious, but they’ve got the exemplary to backmost it up. Awfis isn’t conscionable focused connected Tier-1 cities similar Mumbai and Delhi. They’ve besides moved aggressively into Tier-2 markets similar Guwahati, Chandigarh, and Indore.

Why? Because these smaller cities are wherever the existent maturation is happening. As companies grow beyond metros, they request ready-to-go offices, and Awfis is perfectly positioned to conscionable this demand.

And past there’s the aboriginal of enactment itself. Post-pandemic, hybrid enactment models are the norm. Even though this exemplary has walked backmost a little, it’s inactive much hybrid than the pre-pandemic days. Furthermore, galore companies don’t privation to fastener themselves into semipermanent leases for monolithic bureau spaces anymore. Instead, they similar a premix of imperishable offices and flexible spaces — a strategy often called ‘core + flex’. Awfis is simply a earthy acceptable for this trend, offering businesses the flexibility they request without the hassle of managing day-to-day operations.

So, if you’re thinking, “This sounds great, but what’s the catch?” Well, determination are challenges. Competition is fierce, with players similar Tablespace, WeWork India, and Indiqube besides expanding rapidly. Then there’s the hazard of oversupply successful immoderate markets oregon economical slowdowns affecting occupancy rates. However, Awfis’s managed aggregation exemplary helps it navigate these risks amended than most.

The fiscal motor down the flex revolution

Behind the aesthetics, there’s a superior fiscal motor driving Awfis’s meteoric rise.

Let’s interruption it down to recognize wherever Awfis is today, however it’s performing, and, much importantly, however precocious its valuation tin go.

Revenue growth: More than conscionable seats

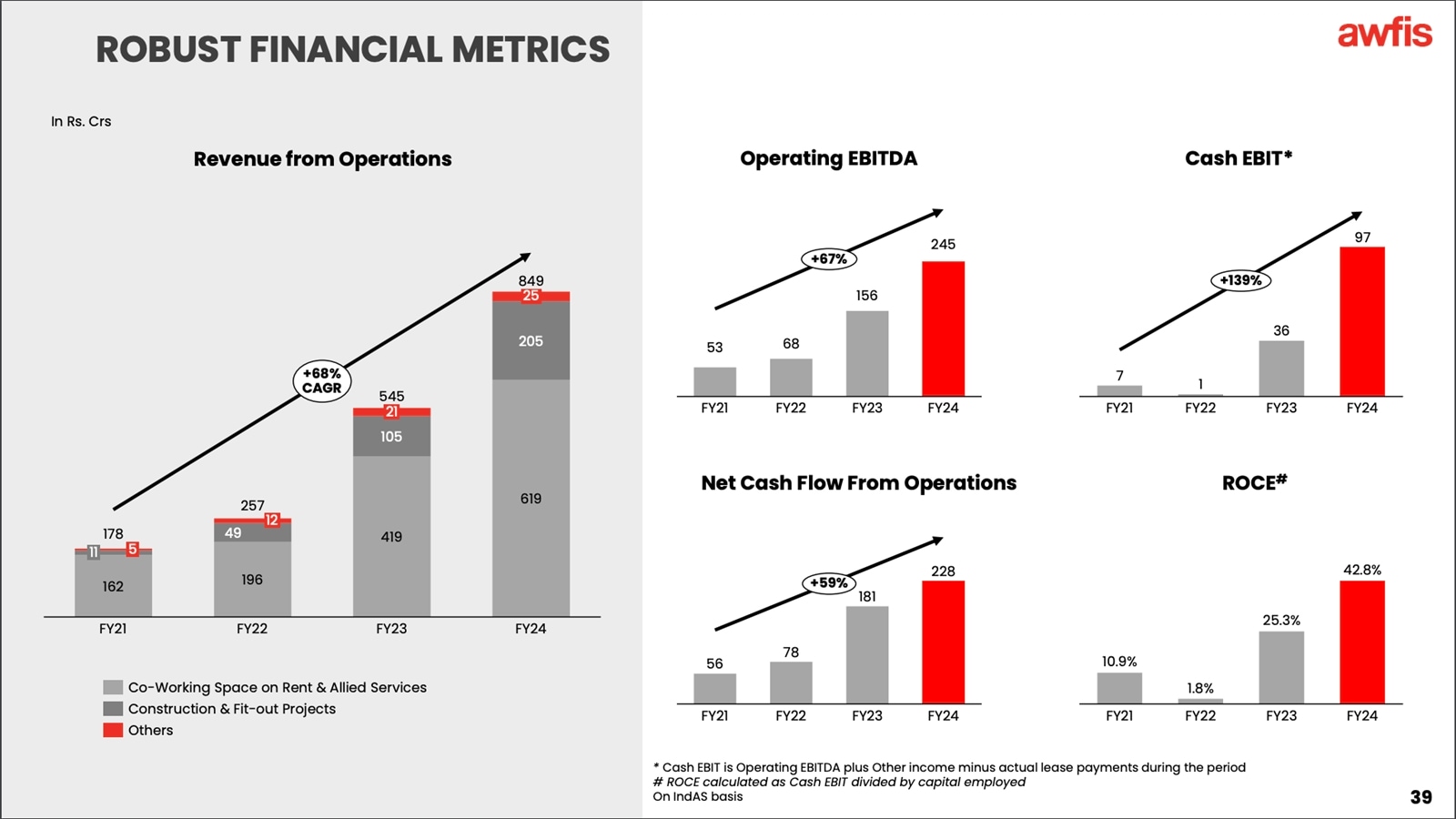

Awfis has been successful hyper-growth mode. In FY23, it posted gross of ₹545 crore. By FY24, this surged by 56% to ₹849 crore. But this isn’t conscionable astir selling much desks. Awfis’s gross streams are becoming much diversified and lucrative.

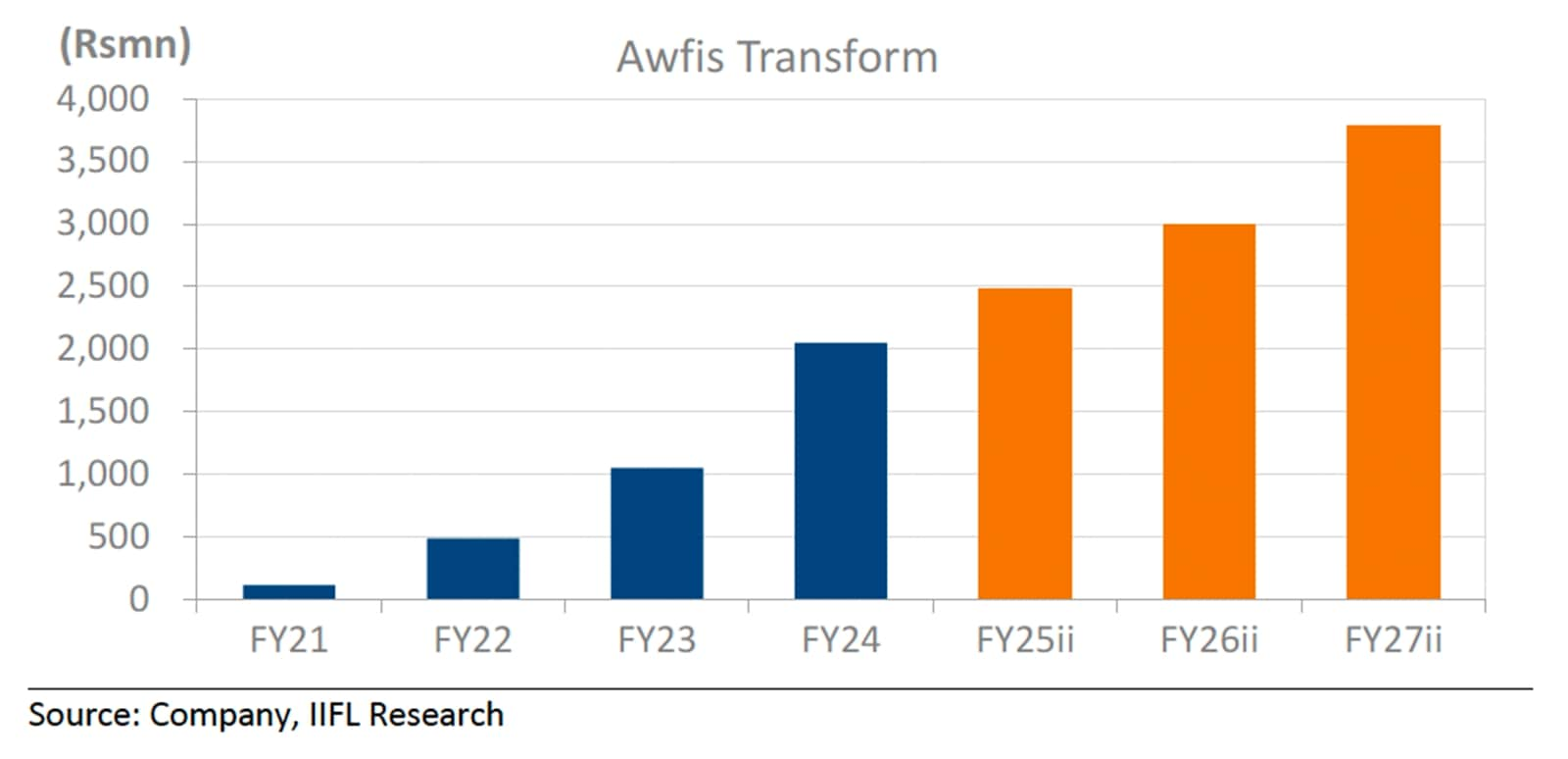

Beyond spot rentals, which inactive relationship for Awfis Transform a bulk of its income, Awfis has tapped into ancillary services (like its design-and-build arm), which handles everything from readying bureau layouts to executing the interior fit-outs, creating afloat customised workspaces for businesses.

Transform unsocial is projected to turn astatine a 23% CAGR, doubling its publication to wide gross by FY27. This dual-engine attack ensures that gross maturation isn’t overly reliant connected occupancy rates alone.

Awfis Transform gross projection. (Source: IIFL Research)

Awfis Transform gross projection. (Source: IIFL Research)

Also, Awfis’s wide gross is expected to beryllium astir ₹2,200 crore by FY27. For perspective, this means astir a 160% maturation successful conscionable 3 years.

Margins that talk for themselves

One of the biggest critiques of coworking companies globally has been their razor-thin margins — oregon deficiency thereof.

Awfis, however, is flipping the script. EBITDA margins, which stood astatine 28.5% successful FY23, are expected to steadily ascent to ~38% by FY27. How is this possible?

Awfis’s fiscal metrics. (Source: Annual Report FY24)

Awfis’s fiscal metrics. (Source: Annual Report FY24)

Operational Efficiency: Awfis’s managed aggregation exemplary drastically reduces superior costs. Unlike accepted coworking players that instrumentality connected hefty leases, Awfis partners with landlords who enarthrosis 50–90% of the fit-out expenses. This not lone minimises upfront concern but besides accelerates payback periods (16 months versus the manufacture mean of 36 months).

Mature Centres Performing Better: As its centers mature (typically wrong 12 months), occupancy rates stabilise astatine astir 85%, improving gross per quadrate foot. This has a nonstop interaction connected margins, arsenic fixed costs stay changeless portion revenues rise.

Premiumisation: Offerings similar Awfis Gold and Elite are aimed astatine higher-paying clients, which boosts per-seat realisations. For example, portion modular Awfis seats make revenues of ₹8,000 per month, premium formats tin fetch 25-40% more.

How Awfis stacks up against the competition

India’s coworking marketplace is fragmented, with implicit 440 operators. Yet, Awfis is starring the complaint with a marketplace stock expected to turn from 7% successful FY23 to 12% by FY27. Here’s however they’re pulling ahead:

Focus connected Tier-2 Cities: While competitors scramble for metro markets, Awfis is making inroads into underserved Tier-2 cities similar Guwahati and Chandigarh. These cities are increasing faster than Tier-1 markets, with request surging astatine a 25% CAGR.

Landlord-Friendly Model: The Managed Aggregation attack allows Awfis to standard faster and mitigate occupancy risks, a important vantage implicit straight-lease competitors similar WeWork India.

Valuation: Is 100% upside possible?

Awfis is presently valued astatine ₹5,000 crore (~$0.5 billion), which, for a institution increasing this fast, feels modest. To fig retired if Awfis could treble its value, let’s interruption it down successful simpler terms.

What is EV/EBITDA and wherefore does it matter?

EV/EBITDA stands for Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization. It’s a fashionable mode to measurement however costly oregon inexpensive a institution is compared to its earnings. Think of it arsenic a mode to fig retired if a company’s worth (enterprise value) makes consciousness based connected however overmuch wealth it’s making.

Right now, Awfis trades astatine an EV/EBITDA aggregate of ~60x for FY24. This means investors are valuing the institution astatine 60 times its expected profits earlier taxes and different costs. While this mightiness dependable high, it’s not antithetic for companies increasing their profits arsenic rapidly arsenic Awfis to commercialized astatine higher multiples.

If prices bash not determination immoderate further, this is apt to beryllium successful the scope of 35x by the extremity of this twelvemonth arsenic the net volition beryllium higher than that of the past year.

For comparison, planetary coworking giants similar IWG (a UK-based flexible workspace leader) person traded astatine multiples of 30-35x during their highest maturation years.

The lawsuit for a ₹10,000 crore valuation

Here’s what would request to happen:

Revenue Growth: Awfis’s gross is projected to turn from ₹849 crore successful FY24 to ~₹2,200 crore by FY27. This benignant of maturation sets the signifier for a higher valuation.

Stronger Profit Margins: Awfis’s EBITDA margins — basically, however overmuch nett it makes earlier definite costs — are expected to amended from 28% successful FY24 to sub-40% successful the adjacent 3 years. As margins improve, the institution becomes much profitable, which justifies a higher valuation.

Dominance successful Tier-2 Cities: Awfis has an aboriginal pb successful smaller cities similar Chandigarh and Guwahati, which are increasing faster than metros. If this strategy pays off, it could importantly boost gross and marketplace share.

Awfis has positioned itself arsenic a frontrunner successful India’s flexible workspace market. With disciplined financials, a astute maturation model, the way up looks promising. While challenges remain, Awfis’s quality to equilibrium maturation with profitability makes it a standout player.

The large question isn’t if Awfis tin turn — it’s however much. If they proceed executing astatine this pace, a valuation of ₹10,000 crore by FY27 isn’t conscionable imaginable — it’s probable. For investors and marketplace watchers, Awfis isn’t conscionable a institution to follow; it’s 1 to keenly track.

Having said that the existent valuations, which are steep, permission nary country for error. Perhaps they already origin successful astir each the positives, which could lone marque the aboriginal travel of the banal much volatile with everyone keenly watching for immoderate signs of slippages. On the different hand, it volition beryllium the affirmative surprises, if any, which could further propel the banal price.

The different large chartless present is however the aggravated contention volition play retired from present on. Lucrative margins and precocious maturation prospects are lone going to marque it much appealing for bigger bets to beryllium placed successful this sector, further intensifying competition. Whether Awfis tin proceed to bushed its competitors and travel retired connected top, portion protecting its margins, volition beryllium 1 happening to keenly ticker retired for.

How they woody with this volition beryllium whether Awfis turns retired to beryllium Aw-esome oregon Aw-ful for its investors.

Note: We person relied connected information from the yearly study and manufacture reports for this article. For forecasting, we person utilized our assumptions.

Parth Parikh has implicit a decennary of acquisition successful concern and research, and helium presently heads the maturation and contented vertical astatine Finsire. He has a keen involvement successful Indian and planetary stocks and holds an FRM Charter on with an MBA successful Finance from Narsee Monjee Institute of Management Studies. Previously, helium has held probe positions astatine assorted companies.

Disclosure: The writer and his dependents bash not clasp the stocks discussed successful this article.

The website managers, its employee(s), and contributors/writers/authors of articles person oregon whitethorn person an outstanding bargain oregon merchantability presumption oregon holding successful the securities, options connected securities oregon different related investments of issuers and/or companies discussed therein. The contented of the articles and the mentation of information are solely the idiosyncratic views of the contributors/ writers/authors. Investors indispensable marque their ain concern decisions based connected their circumstantial objectives, resources and lone aft consulting specified autarkic advisors arsenic whitethorn beryllium necessary.

Discover the Benefits of Our Subscription!

Stay informed with entree to our award-winning journalism.

Avoid misinformation with trusted, close reporting.

Make smarter decisions with insights that matter.

Choose your subscription package

.png "indianexpress.")

.png "khaleejtimes")

.png "arabnews")

English (US) ·

English (US) ·  Hindi (IN) ·

Hindi (IN) ·