14 hours ago

1

14 hours ago

1

The satellite of Indian concern is arsenic intriguing arsenic the emergence of Religare Enterprises.

Over the past 3 years, the banal has delivered a coagulated 100% instrumentality to shareholders, outperforming the Nifty by a wide margin. But the existent enactment lies successful the ongoing bidding warfare for its crown jewel, Care Health Insurance (CHI).

The saga began successful September 2023 erstwhile the Burman family, promoters of Dabur India, launched an unfastened connection to get an further 26% involvement successful Religare astatine ₹235 per share. The Burmans, already holding 21.5%, argued that their connection was a just valuation for a institution amid a turnaround. But Religare’s committee rejected the bid, calling it “undervalued”.

Enter Digvijay ‘Danny’ Gaekwad, a US-based entrepreneur who countered with a ₹275/share bid — a 17% premium to the Burmans’ offer. Gaekwad’s proposal, though legally contested for missing SEBI’s 15-day window, has added substance to the fire, with some sides present locked successful a conflict for control.

The reply lies successful CHI, Religare’s astir invaluable asset. India’s second-largest standalone wellness insurer, CHI has been increasing astatine a blistering pace, with premiums up 25% year-over-year to ₹7,022 crore successful FY24 and a best-in-class claims ratio of 58% (vs. the manufacture mean of 70%). Its impending IPO, targeting a valuation of up to ₹15,000 crore, could beryllium a game-changer for Religare’s shareholders.

Yet, the question remains: Can Religare prolong its 100% instrumentality streak, oregon is the banal moving retired of steam? Let’s dive into the numbers, the context, and the risks.

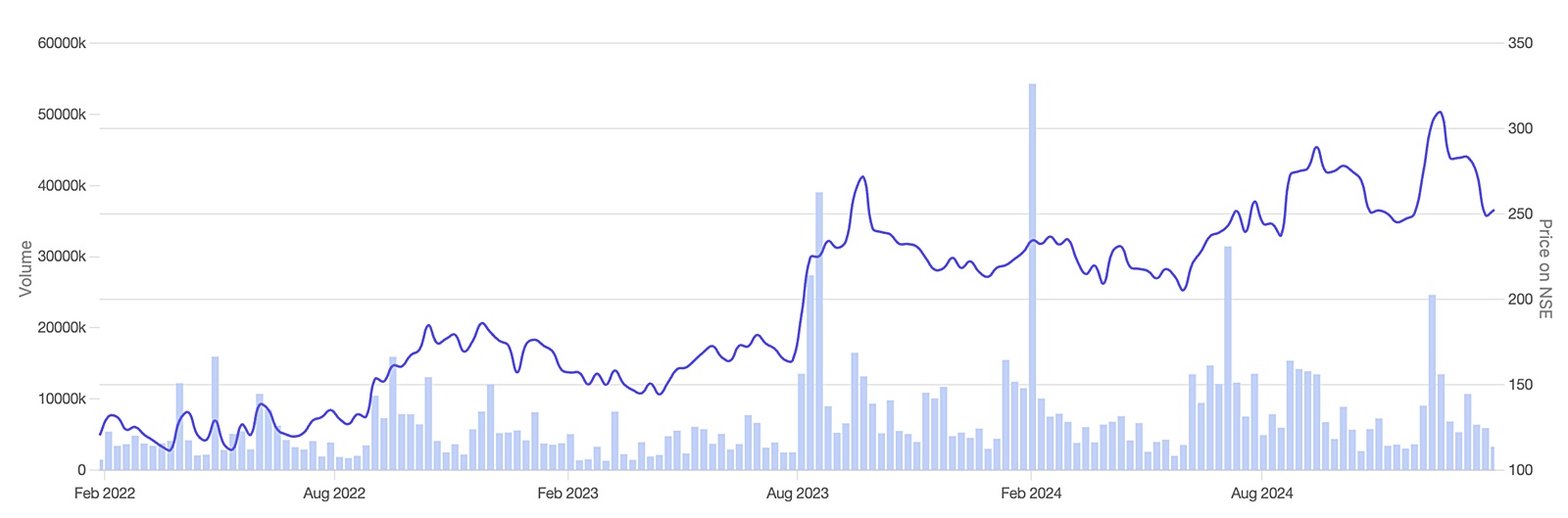

Stock terms question of Religare Enterprises Ltd. (Source: Screener.in)

Stock terms question of Religare Enterprises Ltd. (Source: Screener.in)

The 100% return: What drove it?

Story continues beneath this ad

Religare Enterprises’ 100% instrumentality implicit the past 3 years is simply a communicative of strategical reinvention, a booming security business, and a revival of its fiscal services arm. But beyond the header numbers lies a nuanced communicative of execution, marketplace positioning, and untapped potential. Let’s analyse the cardinal drivers of this turnaround and what they mean for the future.

1. Care Health Insurance (CHI): The motor of growth

Care Health Insurance is the backbone of Religare’s valuation. Here’s why:

Market Positioning and Growth: CHI has carved retired a niche successful India’s wellness security market, which is increasing astatine 14% annually owed to rising healthcare costs and expanding awareness. With a 7% marketplace share, CHI is 2nd lone to Star Health, but its maturation trajectory is arguably much impressive.

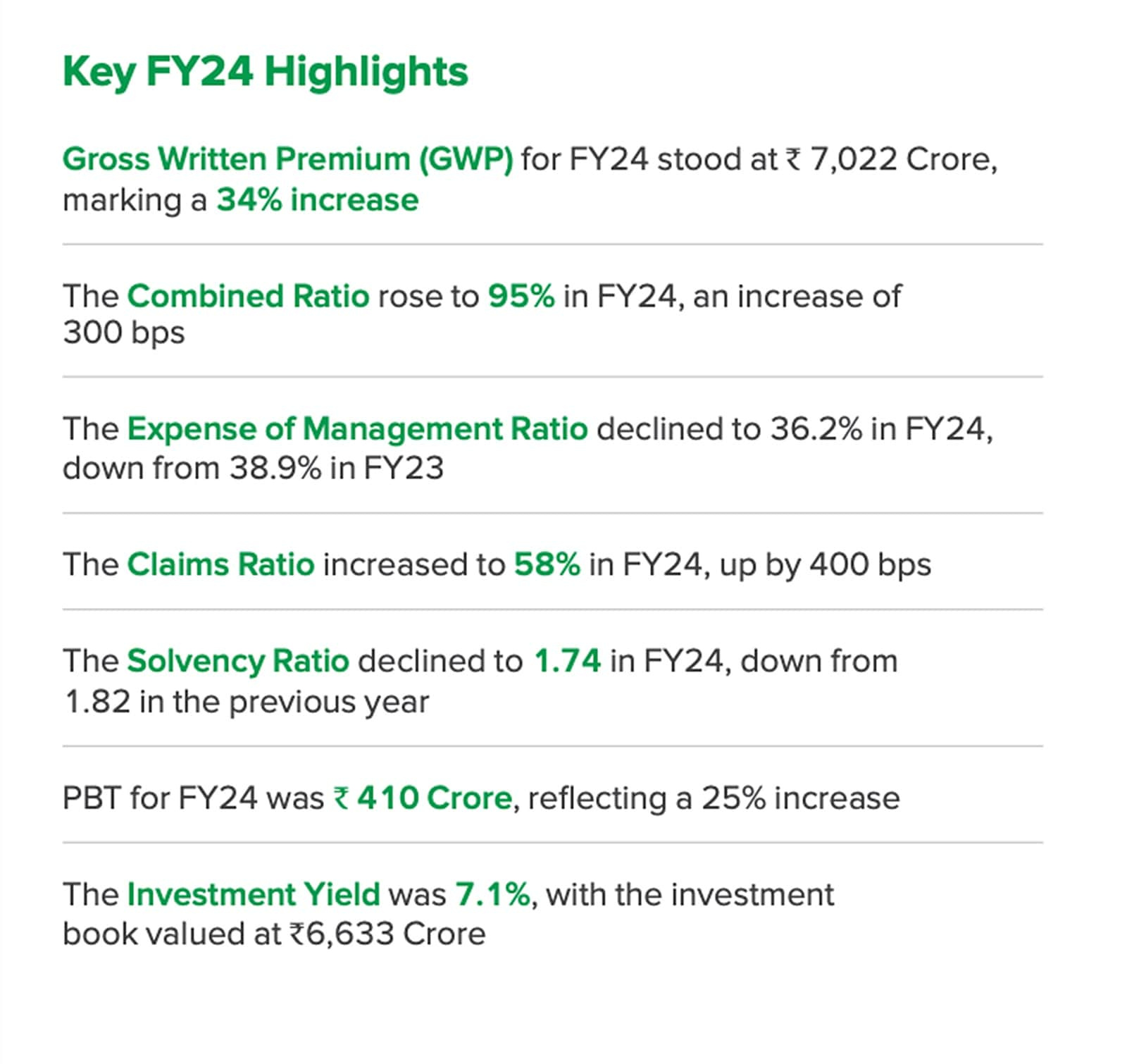

CHI FY24 Highlights. (Source: Religare Annual Report FY24)

CHI FY24 Highlights. (Source: Religare Annual Report FY24)

Premiums grew 34% year-over-year to ₹7,022 crore successful FY24, outpacing the manufacture mean of 14%.

What sets CHI isolated is its operational efficiency.

Story continues beneath this ad

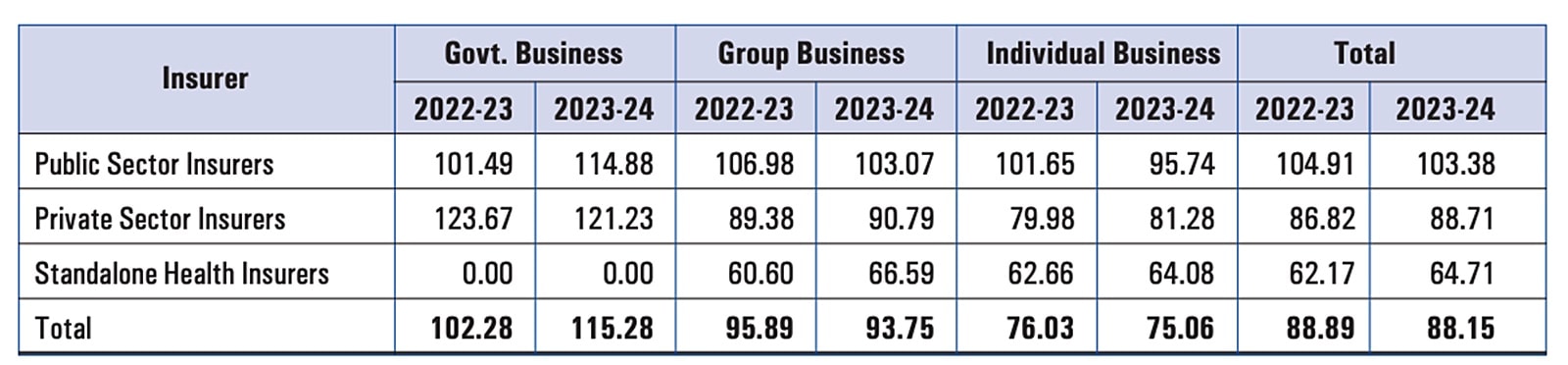

Its claims ratio of 58% (versus the manufacture mean of 88%) reflects superior underwriting and outgo management. This has translated into robust profitability, with pre-tax profits rising to ₹410 crore successful FY24, up from ₹320 crore successful FY23.

Claims Ratio nether Health Insurance Business of General and Health Insurers (in%)

Claims Ratio nether Health Insurance Business of General and Health Insurers (in%)

IPO and valuation upside: Religare Enterprises is gearing up to database CHI, aiming for a valuation of astir ₹15,000 crore, which translates to a price-to-book worth (P/BV) ratio of astir 6x.

At this valuation, Religare’s 63% involvement successful CHI would beryllium valued astatine ₹9,500 crore, surpassing its existent marketplace capitalization of ₹8,100 crore. This upcoming IPO is not simply a liquidity lawsuit but besides serves arsenic a testament to CHI’s maturation imaginable and could enactment arsenic a important catalyst for Religare’s stock.

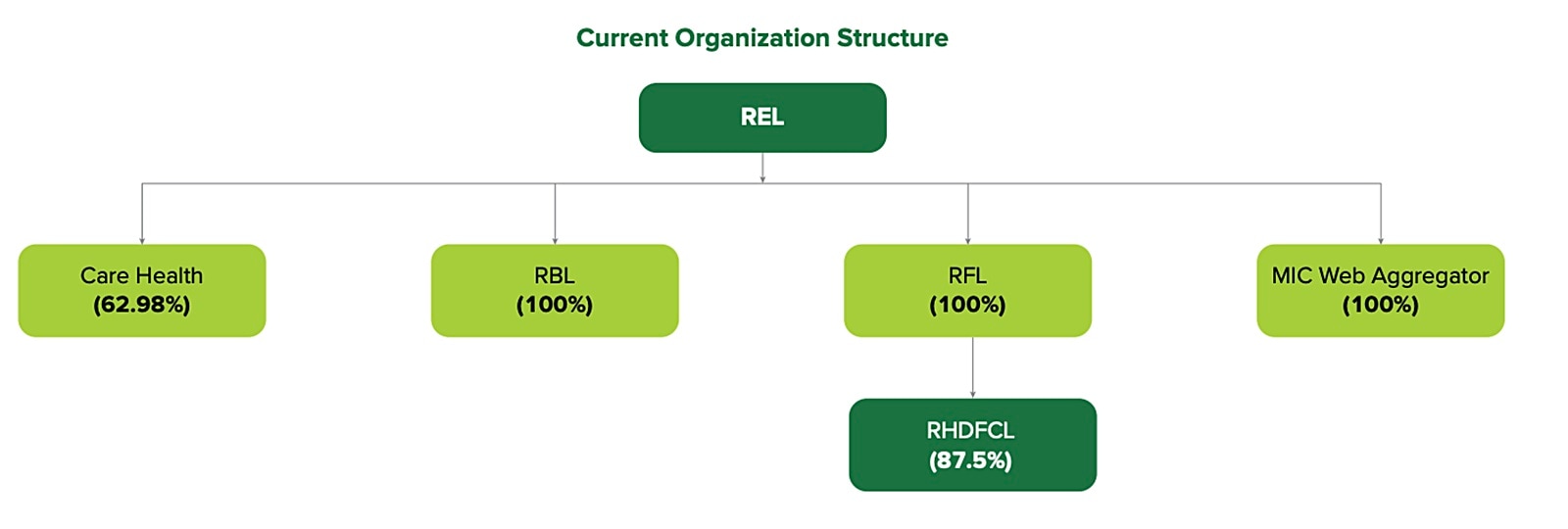

Religare’s Organization Structure. (Source: Religare Annual Report FY24)

Religare’s Organization Structure. (Source: Religare Annual Report FY24)

In the Indian wellness security sector, P/BV ratios alteration among cardinal players.

Story continues beneath this ad

For instance, Star Health and Allied Insurance Company had a P/BV ratio of astir 4x, with a marketplace capitalization of ₹26,000 crore and a publication worth of ₹6,600 crore.

On the different hand, Niva Bupa Health Insurance Company had a P/BV ratio of 5.1x, with a marketplace capitalization of ₹14,000 crore.

These figures bespeak that CHI’s targeted P/BV ratio of 6x positions it competitively wrong the industry, suggesting a balanced valuation that reflects its marketplace lasting and maturation prospects.

CHI’s anticipated occurrence is intimately linked to India’s underpenetrated wellness security market. With lone astir 4% of Indians presently covered by wellness insurance, the imaginable for maturation is substantial. However, the marketplace is becoming progressively competitive, with companies similar Star Health and Niva Bupa actively expanding their footprints. CHI’s quality to prolong its debased claims ratio and proceed its premium maturation volition beryllium important successful maintaining its competitory edge.

2. Religare Broking: Riding India’s retail concern wave

Story continues beneath this ad

While CHI steals the spotlight, Religare’s broking limb has softly go a cardinal contributor to its turnaround.

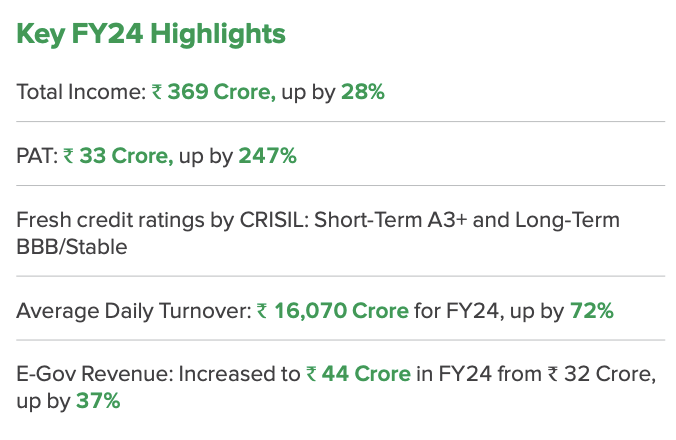

The Retail Trading Boom: India’s equity markets person seen a seismic shift, with retail investors present dominating regular trading volumes. Religare Broking has capitalized connected this trend, increasing gross by 28% YoY to ₹368 crore successful FY24. Net profits much than doubled to ₹33 crore, up by 247% YoY.

Religare Broking FY24 Highlights. (Source: Religare Annual Report FY24)

Religare Broking FY24 Highlights. (Source: Religare Annual Report FY24)

What’s driving this growth? Religare’s absorption connected Tier-2 and Tier-3 cities, wherever fiscal literacy and disposable incomes are rising, has been a game-changer. Its tech-driven level and personalised services person helped it basal retired successful a crowded market.

The broking concern faces stiff contention from discount brokers, which person captured important marketplace stock with their low-cost models. Religare’s quality to differentiate itself done value-added services (e.g., research, advisory) volition beryllium cardinal to sustaining growth.

Story continues beneath this ad

Currently, Religare Broking is apt to beryllium valued astatine astir ₹1,800 crore, equating to a gross aggregate of 5x. This valuation appears blimpish erstwhile compared to manufacture standards. For instance, the mean gross aggregate for brokers is astir 10x.

If Religare tin proceed to standard its broking operations and leverage its strengths successful emerging markets, the concern could germinate into a standalone plus of important value, further enhancing the wide valuation of Religare Enterprises.

3. Debt simplification and lodging concern turnaround

The institution has achieved a singular alteration successful gross debt, reducing it from ₹2,900 crore successful FY20 to ₹678 crore successful FY24. This important simplification has not lone enhanced Religare’s fiscal flexibility but besides restored capitalist confidence.

Notably, Religare Finvest Ltd. (RFL), a wholly-owned subsidiary, has go outer debt-free aft completing a One-Time Settlement (OTS) with its lenders, clearing implicit ₹9,000 crore successful debt.

Story continues beneath this ad

Housing Finance and SME Lending: Religare’s lodging concern part returned to profitability successful FY24, marking a important turnaround aft years of losses. Although presently a smaller contributor to the company’s wide performance, this part holds potential, particularly successful the discourse of India’s recovering existent property market.

Religare Finvest, the company’s SME lending arm, has besides achieved a debt-free presumption successful FY24 and is awaiting regulatory support from the Reserve Bank of India (RBI) to resume operations.

Given India’s important MSME recognition gap, estimated astatine $530 billion, successfully revitalizing this concern conception could presumption it arsenic a important maturation operator for Religare.

Investment Portfolio: As of FY24, Religare’s concern portfolio is valued astatine ₹6,633 crore, encompassing stakes successful entities specified arsenic SMC Insurance and different fiscal assets.

Story continues beneath this ad

This diversified portfolio provides the institution with liquidity options for aboriginal maturation initiatives oregon further indebtedness reduction, adding an further furniture of worth to its fiscal structure.

Religare’s equilibrium expanse cleanup has been a captious origin successful its banal rally.

Can further upside beryllium possible?

Let’s interruption it down.

The upcoming IPO of CHI is simply a important event. With an anticipated valuation of ₹15,000 crore, Religare’s 63% involvement would beryllium worthy astir ₹9,450 crore.

Even if the IPO doesn’t materialise, CHI’s valuation remains robust, perchance exceeding that of its genitor company. It’s worthy noting that genitor companies often commercialized astatine a discount, sometimes astir 25%, owed to factors similar conglomerate discount. Even with specified a discount, the worth of Religare’s involvement successful CHI could inactive surpass its existent marketplace headdress of astir ₹8,100 crore.

Then there’s Religare Broking.

With a reported gross of ₹368 crore successful FY24 and applying a blimpish 5x gross multiple, we’re looking astatine a valuation of astir ₹1,840 crore.

Don’t hide the concern portfolio, valued astatine ₹6,633 crore arsenic of FY24, which includes stakes successful entities similar SMC Insurance.

Adding these up, we get a full valuation of astir ₹18,000 crore. That’s much than treble the existent marketplace capitalization. This suggests that the marketplace mightiness beryllium undervaluing Religare’s assets, indicating imaginable upside for investors.

Of course, it’s indispensable to support successful caput the associated risks, specified arsenic regulatory approvals, marketplace competition, and execution challenges. But fixed the numbers, determination seems to beryllium a compelling lawsuit for further growth.

So, is determination much upside? The figures suggest determination could be. As always, it’s important to bash thorough probe and see each factors earlier making concern decisions.

Note: We person relied connected information from the yearly reports passim this article. For forecasting, we person utilized our assumptions.

Parth Parikh has implicit a decennary of acquisition successful concern and research, and helium presently heads the maturation and contented vertical astatine Finsire. He has a keen involvement successful Indian and planetary stocks and holds an FRM Charter on with an MBA successful Finance from Narsee Monjee Institute of Management Studies. Previously, helium has held probe positions astatine assorted companies.

Disclosure: The writer and his dependents bash not clasp the stocks discussed successful this article.

The website managers, its employee(s), and contributors/writers/authors of articles person oregon whitethorn person an outstanding bargain oregon merchantability presumption oregon holding successful the securities, options connected securities oregon different related investments of issuers and/or companies discussed therein. The contented of the articles and the mentation of information are solely the idiosyncratic views of the contributors/ writers/authors. Investors indispensable marque their ain concern decisions based connected their circumstantial objectives, resources and lone aft consulting specified autarkic advisors arsenic whitethorn beryllium necessary.

.png "indianexpress.")

.png "khaleejtimes")

.png "arabnews")

English (US) ·

English (US) ·  Hindi (IN) ·

Hindi (IN) ·