3 hours ago

1

3 hours ago

1

EID Parry has agelong been a dependable beingness successful the marketplace — a institution that has softly built its bequest implicit the years.

Its travel whitethorn look unassuming astatine first: implicit the past 5 years, it has delivered a respectable 29% yearly instrumentality (CAGR), and today, it is valued astatine astir ₹15,000 crore. But beneath this humble marketplace headdress lies a astonishing twist.

EID Parry holds a 56% involvement successful Coromandel International, a starring sanction successful the agri-chemicals sector, with a full marketplace headdress of ~₹56,000 crore.

EID Parry’s involvement successful Coromandel International. (Source: Coromandel’s AR FY24)

EID Parry’s involvement successful Coromandel International. (Source: Coromandel’s AR FY24)

In elemental terms, successful EID’s books, this involvement successful Coromandel unsocial is worthy astir ₹31,000 crore — much than treble EID Parry’s full marketplace value.

This striking opposition raises an important question: Is the marketplace afloat recognising the existent imaginable of EID Parry? While its header numbers mightiness suggest a dependable performer, the hidden treasure successful its portfolio hints astatine a overmuch larger story, 1 wherever important upside could beryllium waiting to beryllium unlocked.

Stock terms question of EID Parry (India) Ltd. (Source: Screener.in)

Stock terms question of EID Parry (India) Ltd. (Source: Screener.in)

Unveiling the hidden 250%: EID Parry’s underlying transformation

EID Parry has built its bequest connected solid, accepted businesses that person weathered marketplace cycles with dependable performance. Over the past 5 years, its halfway operations — chiefly successful sweetener accumulation and nutraceuticals — person provided the stableness and currency travel that signifier the backbone of the company.

1. Sugar: The aged reliable

Story continues beneath this ad

Sugar has agelong been the bedrock of EID Parry’s operations.

With six modern mills crossed South India and a combined cane crushing capableness of astir 40,800 tonnes per day, the sweetener concern remains a steadfast, if not flashy, contributor.

In FY24, the sweetener conception generated astir ₹1,865 crore successful revenue. However, this concern isn’t without its challenges. Regulatory interventions, specified arsenic export restrictions, mandated cane pricing, and government-imposed blending targets, often compression margins into sub 6% range.

2. Co-generation: Turning byproducts into power

Story continues beneath this ad

The co-generation concern takes what mightiness different beryllium a discarded merchandise — bagasse, the fibrous residue from sugarcane — and transforms it into a invaluable asset.

EID Parry’s integrated sweetener mills are equipped with cogeneration units that unneurotic nutrient astir 140 MW of power. This conception not lone meets the interior vigor needs of the mills but besides generates surplus electricity, which is sold to the grid oregon backstage players.

Though the gross figures for co-generation are smaller compared to sweetener (contributing a steady, supportive income stream), the concern has evolved arsenic a captious portion of the sustainability puzzle.

3. Distillery: Fueling maturation with ethanol

The distillery concern is wherever EID Parry leverages its halfway commodity to pat into the high-growth greenish vigor sector.

Story continues beneath this ad

Operating done 5 distilleries with a existent capableness of 582 KLPD, the distillery conception is liable for producing astir 60 cardinal litres of ethanol annually. In FY24, this conception generated astir ₹799 crore successful revenue.

Ethanol accumulation offers margins — typically successful the sub 7% scope — akin to the sweetener business. The strategical displacement to prioritise ethanol, driven by authorities initiatives to blend ethanol with petrol, has allowed the distillery concern to not lone offset immoderate of the inherent cyclicality of sweetener but besides to enactment arsenic a maturation engine.

4. Nutraceuticals: A dash of health

As user preferences displacement toward wellness and integrated products, EID Parry has branched into the nutraceuticals space.

This segment, though humble successful standard compared to sugar, has garnered attraction for its higher-margin potential. In FY24, nutraceuticals generated astir ₹31 crore successful revenue.

Story continues beneath this ad

Products specified arsenic spirulina tablets and different integrated supplements exemplify the company’s committedness to prime and innovation successful wellness and wellness. While maturation present has been variable, the strategical value of nutraceuticals lies successful diversifying gross streams.

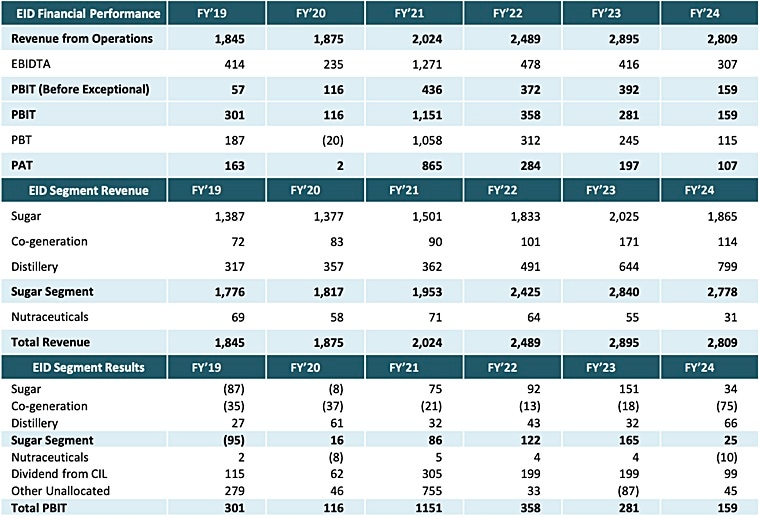

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation May 2024)

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation May 2024)

5. Consumer Products: From bulk to branded

Traditionally known arsenic a bulk sweetener manufacturer, the institution is present positioning itself to seizure the premium retail space. This involves transitioning from selling commoditised sweetener into offering a scope of branded products, specified arsenic value-added sweeteners, supergrains, and different processed nutrient items.

Though inactive successful its nascent stage, the user products conception is rapidly progressing. Recent initiatives see the motorboat of branded sweeteners and packaged supergrains that purpose to pat into the fast-growing Indian FMCG market.

Story continues beneath this ad

By expanding its organisation — from a fewer 1000 outlets to implicit 1 lakh retail touchpoints — the institution is moving to unafraid a much profitable and resilient gross base. This displacement is designed to unlock premium pricing and trim the dependency connected fluctuating commodity prices, signaling a caller section successful EID Parry’s agelong history.

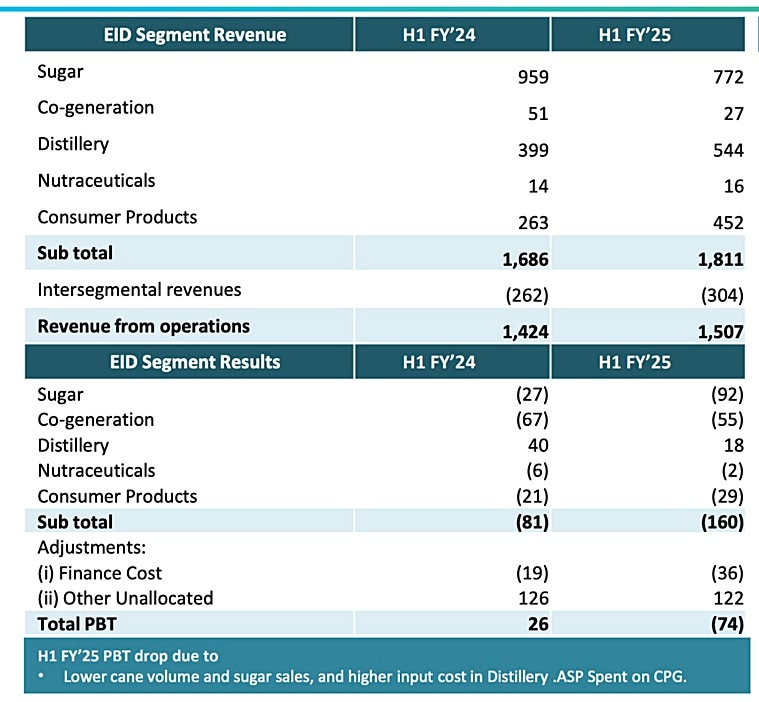

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation Nov 2024)

EID Parry’s Segmental Rev/Profit Trend. (Source: Investor Presentation Nov 2024)

Valuation analysis: Sum‐of‐the-parts versus marketplace discount

To recognize the disparity betwixt marketplace cognition and cardinal value, we archetypal request to analyse the idiosyncratic components of EID Parry’s business.

The sweetener division, historically the company’s mainstay, continues to make accordant revenues, reporting ₹1,865 crore successful FY24. However, sweetener is an inherently volatile industry, taxable to authorities pricing policies, export restrictions, and unpredictable upwind conditions. Despite these challenges, the concern remains a important portion of India’s cultivation landscape. Globally, sweetener companies commercialized astatine price-to-earnings (P/E) multiples of astir 9x, and adjacent with subdued profitability, EID Parry’s sweetener concern could beryllium conservatively valued astatine ₹300-400 crore.

Story continues beneath this ad

Beyond sugar, EID Parry has been steadily leveraging its by-products.

The co-generation business, which converts bagasse into renewable energy, contributes to operational efficiencies. However, this conception reported a PBIT nonaccomplishment of ₹75 crore successful FY24, reflecting operational inefficiencies oregon non-cash adjustments. While the gross from this conception stood astatine ₹114 crore, its valuation remains subdued, estimated astatine ₹100-200 crore, chiefly based connected aboriginal vigor income imaginable alternatively than existent earnings.

The existent game-changer wrong EID Parry’s halfway operations is its distillery business, which focuses connected ethanol production. With the Indian authorities aggressively pushing for ethanol blending successful substance (targeting 20% by 2026), companies successful this abstraction person witnessed improved pricing powerfulness and margins.

EID Parry’s distillery conception recorded ₹799 crore successful gross successful FY24, supported by tenable margins, making it the astir profitable standalone segment. Globally, ethanol businesses commercialized astatine higher multiples, astir 12x earnings, suggesting a valuation scope of ₹750-900 crore.

Story continues beneath this ad

Then comes the nutraceuticals division, which, contempt its comparatively tiny publication to wide revenue, holds value owed to its higher-margin profile. However, FY24 saw a crisp diminution successful conception profitability, with a PBIT nonaccomplishment of ₹10 crore. This diminution whitethorn beryllium temporary, but it highlights the situation of scaling operations successful India’s fragmented wellness market. Even with fluctuating performance, nutraceuticals thin to pull premium valuations owed to semipermanent request trends, starring to a valuation scope of ₹200-300 crore.

Lastly, EID Parry’s user products conception represents an effort to determination beyond bulk sweetener income into the branded retail space. This shift, if executed well, could let the institution to bid higher pricing powerfulness and amended net stability. Though early-stage, a valuation estimation of ₹300-500 crore tin beryllium assigned, assuming mean traction successful premium sweetener and wellness-based user products.

When aggregated, these halfway concern segments lend to a blimpish standalone valuation of astir ₹3,000 crore, which, portion humble successful isolation, underscores the spot of EID Parry’s diversified operations.

The Coromandel connection: A ₹31,000 crore undervalued asset?

What makes EID Parry unsocial isn’t conscionable its halfway concern — it’s the information that it owns a 56% involvement successful Coromandel International, a ascendant subordinate successful India’s fertiliser and agro-chemicals industry. Over the past 5 years, Coromandel has grown astatine a 24% CAGR, and today, the institution boasts a marketplace capitalisation of ₹56,000 crore. This means that EID Parry’s involvement unsocial is worthy astir ₹31,000 crore, much than treble its ain marketplace capitalisation of ₹15,000 crore.

This monolithic discrepancy is hard to ignore.

If an capitalist were to bargain EID Parry today, they would efficaciously beryllium getting its full sugar, ethanol, co-generation, nutraceuticals, and user concern for free, portion inactive paying little than the afloat worth of its Coromandel stake. Even aft applying a holding institution discount of 50-60%, EID Parry’s just worth should beryllium astatine slightest ₹18,000-22,000 crore, inactive higher than wherever it presently trades.

Why the heavy discount?

The persistent undervaluation of EID Parry tin beryllium attributed to respective cardinal factors:

Holding institution discount

- Holding companies successful India typically commercialized astatine a 50-60% discount owed to concerns implicit superior allocation, deficiency of nonstop power implicit subsidiary currency flows, and the reluctance of absorption to unlock value.

- Investors often similar to bargain Coromandel shares directly, alternatively than purchasing EID Parry and indirectly owning Coromandel.

Cyclicality of the sweetener business

- While EID Parry has been expanding into ethanol, nutraceuticals, and branded user products, the sweetener conception remains volatile.

- The manufacture is highly regulated, with government-imposed cane pricing, ethanol blending mandates, and export restrictions impacting profitability.

Trading liquidity concerns

- While Coromandel trades with a regular measurement of ₹250 crore, EID Parry’s regular trading volumes are lone ₹30-40 crore, making it little charismatic for ample organization investors.

Murugappa Group’s blimpish approach

- The Murugappa family, which owns EID Parry, is known for semipermanent stableness implicit assertive fiscal engineering.

- Historically, they person not pursued spin-offs oregon involvement sales, which frustrates investors looking for near-term catalysts.

The concern opportunity: Is determination wealth to beryllium made?

At its existent marketplace capitalisation of ₹15,000 crore, EID Parry is being valued arsenic if its standalone businesses (sugar, ethanol, co-generation, nutraceuticals, and user products) are hardly worthy anything.

Assuming the standalone businesses are conservatively valued astatine ₹3,000 crore, that leaves the implied valuation of its 56% Coromandel involvement astatine conscionable ₹12,000 crore — a 60% holding institution discount from its just marketplace worth of ₹31,000 crore.

While a 50-60% discount is high, it is not antithetic successful the Indian marketplace for holding companies, particularly those with diversified businesses and a past of blimpish superior allocation. However, for investors to spot meaningful upside, the pursuing triggers would request to materialise:

Narrowing of the holding institution discount

- A partial oregon afloat spin-off of Coromandel International would unit the marketplace to delegate a fairer worth to EID Parry’s stake.

- If Murugappa Group monetises a information of its Coromandel stake, either done involvement merchantability oregon dividend distribution, it could trim the discount significantly.

Ethanol enlargement and higher profitability successful standalone business

- The government’s 20% ethanol blending mandate by 2026 presents a large maturation accidental for the distillery segment.

- If EID Parry’s ethanol gross and margins improve, it would assistance standalone profitability, making the concern much attractive.

Debt simplification and superior restructuring

- EID Parry’s nett indebtedness is manageable, but a further simplification successful indebtedness levels (either done Coromandel dividends oregon operational currency flow) could amended capitalist sentiment.

- A buyback oregon peculiar dividend from Coromandel’s currency travel could besides service arsenic a value-unlocking move.

Conclusion: A heavy worth play that needs a catalyst

At a 60% holding institution discount, EID Parry’s valuation is stretched to the higher extremity of the Indian marketplace range. While specified discounts aren’t abnormal, they bespeak that the marketplace is profoundly sceptical of contiguous worth unlocking.

For investors, the cardinal question is: Will this discount persist, oregon volition 1 of these catalysts trigger a re-rating? If immoderate of the supra scenarios materialise, EID Parry could spot an upside arsenic its discount narrows toward the little extremity of the emblematic holding institution scope (40–50%).

While patience is required, the operation of Coromandel’s dependable growth, ethanol-driven profitability improvements, and imaginable firm restructuring makes EID Parry a deep-value accidental with asymmetric upside. Only clip volition archer whether this thrust towards unlocking volition crook retired to beryllium saccharine arsenic well.

Note: We person relied connected information from the yearly reports passim this article. For forecasting, we person utilized our assumptions.

Parth Parikh has implicit a decennary of acquisition successful concern and research, and helium presently heads the maturation and contented vertical astatine Finsire. He has a keen involvement successful Indian and planetary stocks and holds an FRM Charter on with an MBA successful Finance from Narsee Monjee Institute of Management Studies. Previously, helium has held probe positions astatine assorted companies.

Disclosure: The writer and his dependents bash not clasp the stocks discussed successful this article.

The website managers, its employee(s), and contributors/writers/authors of articles person oregon whitethorn person an outstanding bargain oregon merchantability presumption oregon holding successful the securities, options connected securities oregon different related investments of issuers and/or companies discussed therein. The contented of the articles and the mentation of information are solely the idiosyncratic views of the contributors/ writers/authors. Investors indispensable marque their ain concern decisions based connected their circumstantial objectives, resources and lone aft consulting specified autarkic advisors arsenic whitethorn beryllium necessary.

.png "indianexpress.")

.png "khaleejtimes")

.png "arabnews")

English (US) ·

English (US) ·  Hindi (IN) ·

Hindi (IN) ·